ESS vs. ESOP: What’s the difference?

In Australia, an employee share scheme (ESS) and an employee share option plan (ESOP) are similar in that they both allow eligible workers (employees, contractors or directors) to purchase shares in their employer's company, usually at a favourable price. These schemes aim to incentivise employees to work towards the company's long-term success, as their personal financial interests will be aligned with those of the company. This article explores the differences between an ESS and an ESOP, and the key legal considerations when implementing one of these schemes to retain top talent in your startup.

Employee Share Scheme

An employee share scheme (ESS) is a type of remuneration that allows eligible employees to purchase shares in their employer's company on tax-favourable terms.

The Australian Tax Office (ATO) offers startup tax concessions to companies and employees under an ESS. To be eligible:

-

The shares offered must be ordinary (and not preference) class shares;

-

Workers must pay at least 85% of fair market value unless the safe harbour valuation applies;

-

The shares must not be sold for at least three years;

-

The company must offer shares to at least 75% of its Australian permanent employees who have worked at the business for at least three years; and

-

A single employee cannot own greater than 10% of the company’s shares.

Employee Share Option Plan

An employee share option plan (ESOP) is a type of employee benefit that gives employees the option to purchase shares in their employer's company at a set price in the future. If an employee satisfies all the conditions attached to their options, the employee can exercise their vested options to purchase shares in the company.

Similar to an ESS, an eligible ESOP must follow certain rules:

-

The shares that the options are granted over must be ordinary shares;

-

Workers must pay at fair market value to exercise the options (which, if a company is eligible, may be calculated using the safe harbour valuation methods, which may allow companies to determine the market value by reference to the company’s tangible assets);

-

The options (or shares acquired upon exercise of the options) must not be sold for at least three years; and

-

A single employee cannot own greater than 10% of the company’s shares.

A vesting period is the length of time that an employee must stay with the company before they have the right to exercise their options and purchase the shares. This vesting period aims to incentivise employees to stay with the company long-term and encourage them to work towards its goals. If any vesting conditions are not met, employees may lose the right to those options.

Benefits of Share and Option Schemes

Both an ESS and ESOP can help retain key employees by giving them a sense of ownership and investment in the company. The benefits include:

-

Aligning employee interests with those of the company: When employees have a financial interest in the company, they are more likely to be motivated to work towards its goals;

-

Improving employee retention: Key employees may be more likely to stay with the company if they have the opportunity to purchase shares in the company at a favourable price;

-

Attracting talent: An ESS or ESOP can be an attractive perk for prospective employees, making it easier for the company to attract top talent;

-

Boosting morale: Employees who participate in an ESS or ESOP feel valued and recognised for their contributions to the company, which can improve morale and increase job satisfaction; and

-

Providing a reward for long-term performance: An ESS or ESOP provides employees with a long-term incentive for their contributions to the company.

Differences between an ESS and ESOP

The table below summarises the key differences between the two.

| ESS | ESOP | |

| Participation | Your company must offer shares to at least 75% of its Australian permanent employees who have worked in the company for at least three years. | Your company can offer options to as many or as few participants as it chooses. |

| Treatment of unvested shares | Unvested shares must be bought back by your company and cancelled or redistributed. Alternatively, the unvested shares can be transferred to remaining shareholders. | Unvested options fall away and lapse. The lapsing of the option does not require any payment by the company. |

| Voting rights | Participants are shareholders from day one. They have ordinary voting rights and are entitled to attend and vote at general meetings. This may be a disadvantage, as your company will need to obtain more shareholder consent to pass certain decisions. | Participants are not shareholders until they have exercised their options. As such, they will not have voting rights. This is a benefit of ESOPs, as there are less shareholders to obtain consent from. |

| Dividends | Participants are shareholders, meaning they are entitled to dividends. | As participants are not shareholders, they are not entitled to dividends. |

Other considerations

The ATO provides guidelines for implementing an ESS or ESOP, and companies must comply with all relevant legislation, including the Corporations Act 2001 and the Income Tax Assessment Act 1997. Consulting with a legal and financial professional can help ensure that your ESS or ESOP is structured and administered in compliance with all relevant regulations.

Additionally, under the Corporations Act 2001, a proprietary company is limited to 50 non-employee shareholders. Likewise, a proprietary company with over 50 shareholders (of any type, whether employees or not) will be subject to the Takeover Provisions. As such, a company implementing an ESS or ESOP may risk exceeding the 50-shareholder limit and being subject to additional compliance burdens.

Key takeaways

Retaining top talent is essential to the success and longevity of your startup. However, properly remunerating workers can be difficult if funds are limited. If your startup is struggling to offer workers competitive salaries, consider offering eligible workers an ownership stake in the company on tax-favourable terms. An employee share scheme (ESS) or employee share option plan (ESOP) can allow you to incentivise workers, giving them an ownership stake in your company.

For more information or assistance drafting an ESS or ESOP, LegalVision’s experienced startup lawyers can assist as part of their membership. For a low monthly fee, you will have unlimited access to lawyers to answer your questions and draft and review your documents. Call LegalVision on 1300 544 755 or visit their membership page.

Disclaimer: This article is for informational purposes only and does not constitute a specific product recommendation, or taxation or financial advice and should not be relied upon as such. While we use reasonable endeavours to keep the information up-to-date, we make no representation that any information is accurate or up-to-date. If you choose to make use of the content in this article, you do so at your own risk. To the extent permitted by law, we do not assume any responsibility or liability arising from or connected with your use or reliance on the content on our site. Please check with your adviser or accountant to obtain the correct advice for your situation.

FURTHER READING

Save time and money by sharing your portfolio with your accountant

It's easy to save time and money at tax time by sharing access to your Sharesight portfolio with your accountant. Keep reading to learn more.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

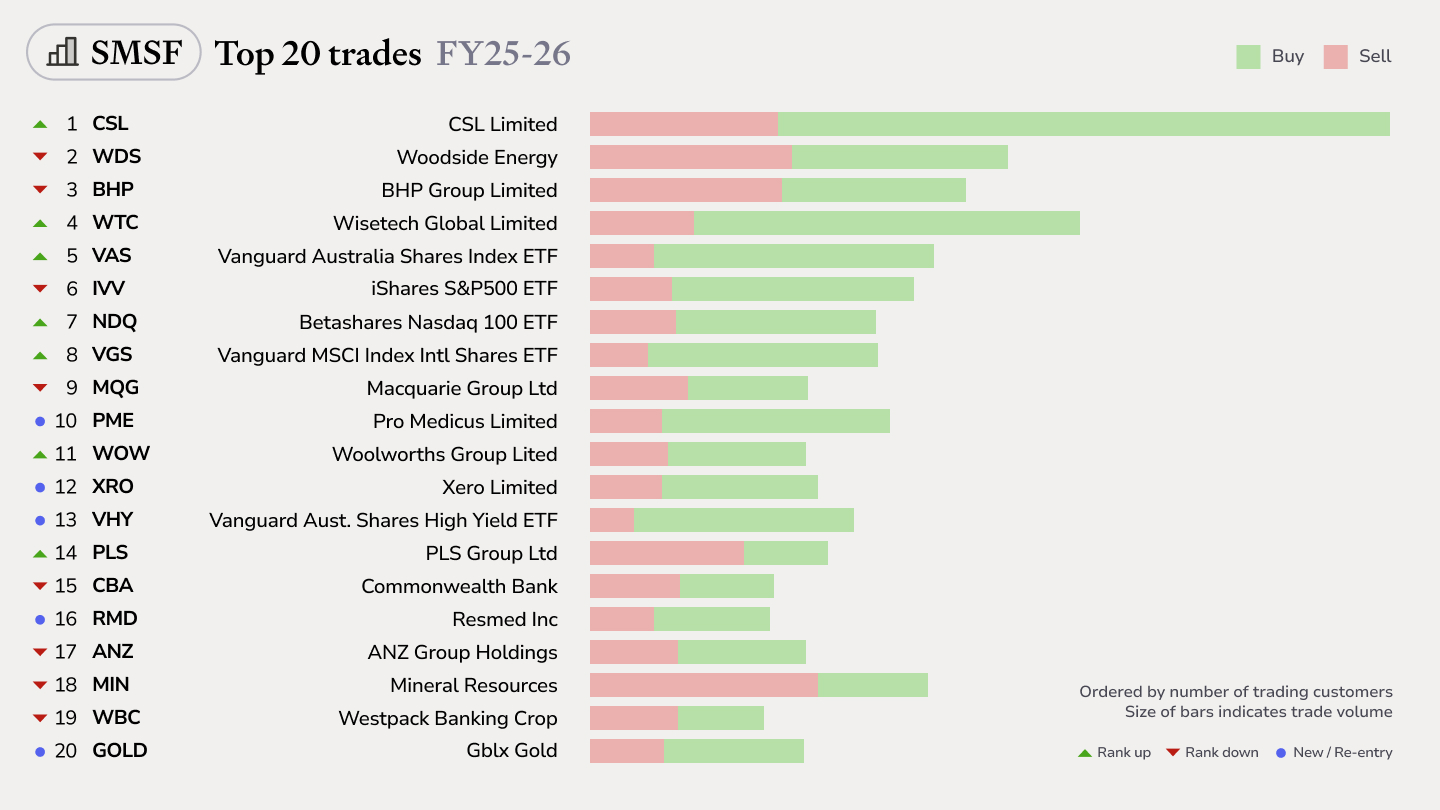

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.