Do you need to diversify your investments?

An article in the Dominion Post on 29 January said “Diversify and beat the retirement cash blues”. It went on to advise that “an effective portfolio is well diversified across different asset classes -- cash, fixed interest, property and shares -- and countries”.

In my view diversification to that extent is more likely to create retirement cash blues than beat them and would not result in a very effective portfolio. For one thing it is not practical for most investors to diversify to the extent recommended unless they invest in managed funds. And the long-term performance of almost all managed funds leaves a lot to be desired. Even a portfolio of randomly selected NZ and Australian shares is likely to out-perform most managed funds, particularly when their fees are taken into account.

Shares and property consistently outperform cash or fixed interest on a long-term basis (and retirement saving is a long-term project) so why would you want to erode your higher-earning share portfolio by diversifying into fixed interest? There are three main reasons often put forward.

First, diversification allows you to spread risk. The hope is that any poor performance will be confined to a small part of your portfolio.

The second reason has to do with liquidity risk. If you need your money urgently, will it be available when you want it and without suffering a loss or an early repayment penalty?

And finally, diversification reduces volatility.

These sound like good reasons to diversify. But are they? The problem with diversification is that while it can limit your losses, it can have a far greater limiting effect on your gains. It dumbs down your investment performance to a low average. As DIY investors we can do much better than that. Remember, the worst you can do is lose 100% your money, but on the other hand the share market gives you plenty of opportunities to earn far more than 100%.

Many people lose sight of the fact that the primary objective of a long-term savings plan should not be to reduce volatility or the risk of loss, but rather, to maximise returns.

There is another problem with diversification. It works on the premise that if one asset class is doing poorly this will be offset by others in your portfolio doing well. Unfortunately the opposite is more likely to be the case. In the last 12 months people have lost money from fixed interest debentures in finance companies and a decline in the share market and property prices are widely tipped to take a tumble as well.

So here’s the big question: Is there a way for the average DIY Kiwi investor to deal with diversification and maximise returns? Can you have your cake and eat it too? I believe you can. I’ll explain how in my next blog post.

This information is not a recommendation nor a statement of opinion. You should consult an independent financial adviser before making any decisions with respect to your shares in relation to the information that is presented in this article.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

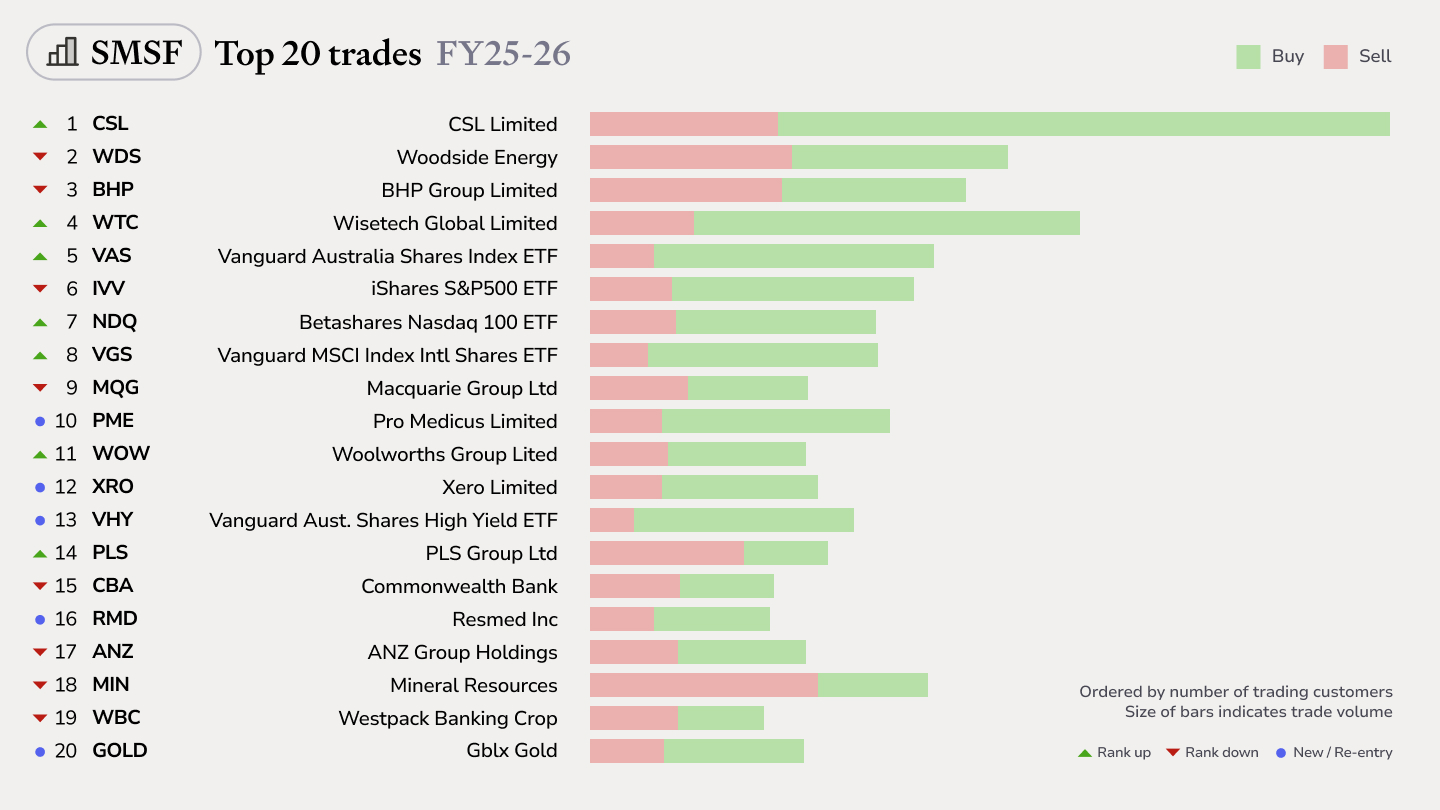

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.

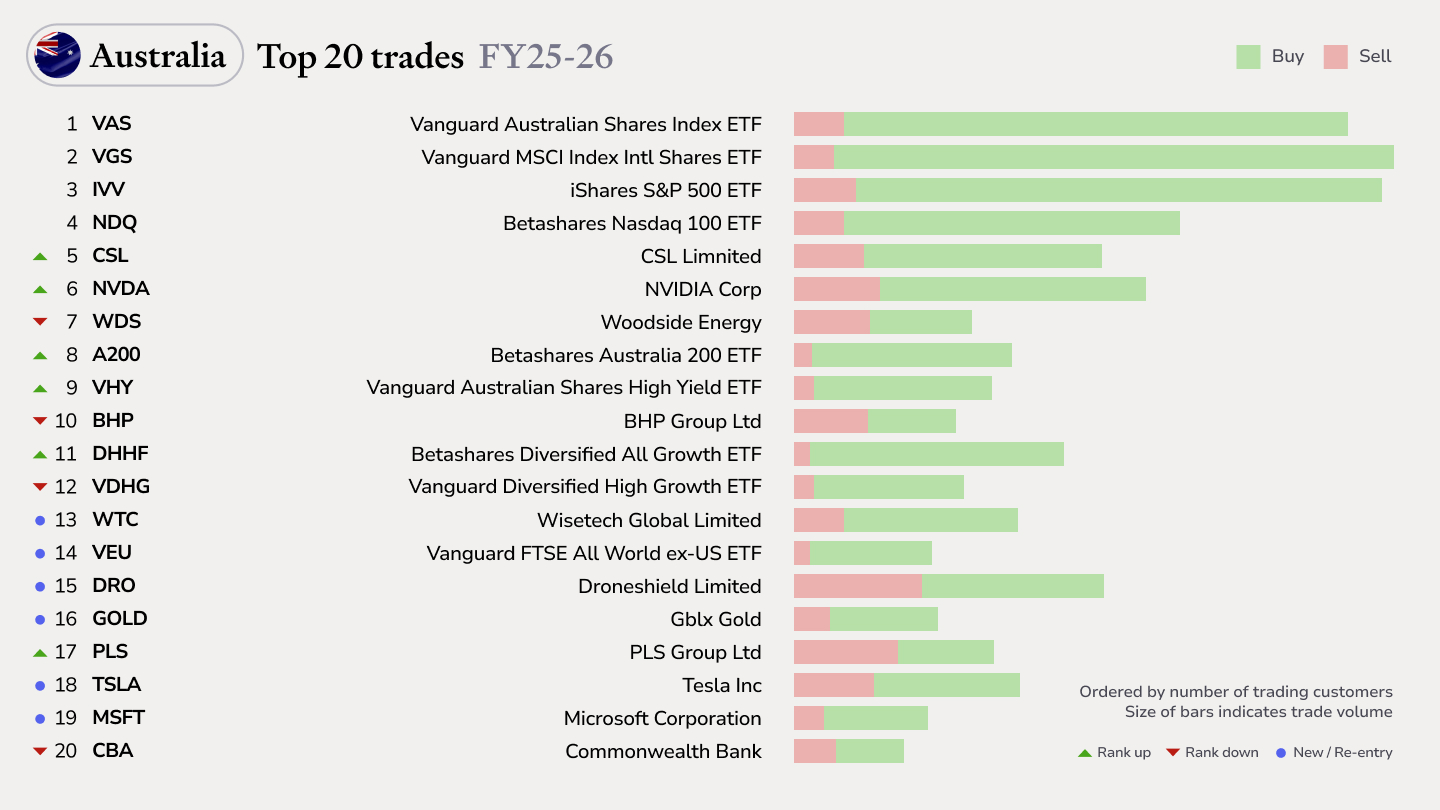

Top trades by Australian Sharesight users in FY25/26

Welcome to the FY25/26 edition of our Australian trading snapshot, where we dive into this financial year’s top trades by Sharesight users.