How much money do you need to save for retirement?

Disclaimer: The below article is for informational purposes only and does not constitute a product recommendation, or taxation or financial advice and should not be relied upon as such. Please consult with your financial adviser or accountant to obtain the correct advice for your situation.

One of the main reasons we invest is to build wealth for retirement. But it’s hard to estimate how much money we’ll need to support our post-work life.

This can be a controversial subject, because different experts and lobby groups can provide very different numbers. However, there is one thing most people agree on: surviving on a pension or Social Security without other forms of savings is hard.

In Australia, Canada, New Zealand and the UK, the maximum payment a single person can receive is low. In the US, which has a fiendishly complicated retirement system, the maximum payment is relatively high at US$36,132, although the average payment is only US$18,036, according to AARP, an association that represents older Americans.

| Country | Maximum annual pension for single person |

| Australia | A$22,110 |

| Canada | C$14,110 |

| New Zealand | NZ$24,722 |

| UK | £6,718 |

| USA | US$36,132 |

So, if you want a comfortable retirement, you’ll need to build wealth during your working years, and to know how much you’ll need by the time you retire, you’ll want to crunch the numbers now to give yourself a nest egg target to guide your investing decisions for the future.

Step 1: Estimate your spending

To calculate how much you might need to save for retirement, the first thing you need to do is estimate how much you expect to spend each year.

Many people assume they’ll spend as much when they’re retired as they do now. However, when you retire, there’s a good chance your cost of living will fall naturally.

You probably won’t have to pay off a mortgage or support children. True, you’ll spend more on doctors, hospitals and pharmaceuticals, but much of that might be covered by health insurance or government subsidies.

It’s important to take stock of your likely expenses during retirement, and build a model using some reasonable assumptions about your expenses during retirement. Vanguard provides a helpful retirement expenses worksheet online that you can work through, or you might prefer your own budgeting spreadsheet (or pencil and paper) to crunch these numbers to arrive at an estimated yearly figure for your expenses in retirement.

The Association of Superannuation Funds of Australia also releases generic expenditure figures based on their own definition of what is a ‘comfortable’ and ‘modest’ retirement lifestyle is that can make a good starting point.

Step 2: Calculate your (median) life expectancy

Once you’ve estimated your likely yearly expenditure, you need to forecast how long you’ll likely spend in retirement.

In the five countries mentioned earlier, life expectancy is about 80 for men and 84 for women.

| Country | Male life expectancy | Female life expectancy |

| Australia | 81.6 | 85.5 |

| Canada | 80.6 | 84.4 |

| New Zealand | 80.7 | 84.0 |

| UK | 79.7 | 83.1 |

| USA | 76.4 | 81.5 |

Source: World Population Review

However, these figures can be misleading, because they refer to the average life expectancy of a person at birth; the average life expectancy of someone who survives until adulthood is higher, and someone who survives until retirement, higher still.

If we look at data from the Australian Government Actuary (AGA) on life expectancy of people who reach age 65, the average (median) 65 year old male can actually expect to live to 88 years, with women expected to live to 90 -- an increase of 6.2 and 4.5 years respectively over the earlier figures.

Step 3: Calculate your target nest egg

Once you’ve estimated how much you expect to spend each year in retirement, you are then in a good place to calculate the size of the nest egg you’ll need to achieve in order to put you in a good position to fund your target lifestyle.

Say for example you were a single Australian woman who had a life expectancy of 90, who planned to retire at 65 and had calculated yearly expenses to fund her lifestyle at $50,000.

While it’s perhaps an overly simplistic calculation, that gives a target of $1,250,000 (25 years in retirement x $50,000 yearly expenditure).

Important caveats

Now first and foremost, this target nest egg is only useful as a starting point to discuss your own circumstances (and you should always consult a financial adviser for individual advice).

There are two important considerations to contextualise the above target number:

Won’t my investments continue to earn returns into retirement?

If you’re an astute investor who benefits from markets that move in the right direction, your investments will hopefully continue to work for you well into your retirement. But that is never guaranteed, and many would consider a defensive portfolio allocation weighted towards relatively safer assets like cash and fixed interest securities (that earn lower returns) appropriate during this phase.

What if I live longer than the median life expectancy?

This is a very important consideration, if you’ve calculated and saved a nest egg to fund your lifestyle based on your median life expectancy, there’s a 50% chance you will live longer than this (and each year you live, your life expectancy increases further). This is known as longevity risk.

To mitigate this risk, some investors turn to products such as annuities that offer regular payments for either a set period, or set payments over your lifetime.

Some may prefer to adopt the "dynamic-spending rule" approach discussed by investment fund manager Vanguard. With a dynamic spending rule approach, investors set a minimum and maximum percentage they are willing to draw down their portfolio each year, and should the portfolio perform poorly, adjust down their budget for spending that year to potentially overdraw the portfolio – leaving less for later years.

The key to succeeding with the dynamic-spending rule approach is having the full picture of your investment portfolio and checking on its performance regularly, that’s where a portfolio tracking tool like Sharesight is critical.

Set on the path to your retirement goals

Once you have a retirement savings goal in mind, the best way to work towards that goal is to take control of your investments now, with an eye to the future. Fortunately Sharesight helps over 100,000 investors around the world do just that. With Sharesight you can:

-

Automatically track your daily price & currency fluctuations, as well as handles corporate actions such as dividends and share splits

-

Run powerful reports built for investors, including Performance, Portfolio Diversity, Contribution Analysis and Future Income (upcoming dividends)

-

Plus run tax reports including Taxable Income (dividends/distributions), Capital Gains Tax (Australia and Canada), Traders Tax (Capital Gains for traders in NZ) and FIF foreign investment fund income reports (NZ)

There’s no time like the present to progress towards your retirement goals. Take the first step today, and sign up for a free Sharesight account to get started.

Retirement calculators

FURTHER READING

Save time and money by sharing your portfolio with your accountant

It's easy to save time and money at tax time by sharing access to your Sharesight portfolio with your accountant. Keep reading to learn more.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

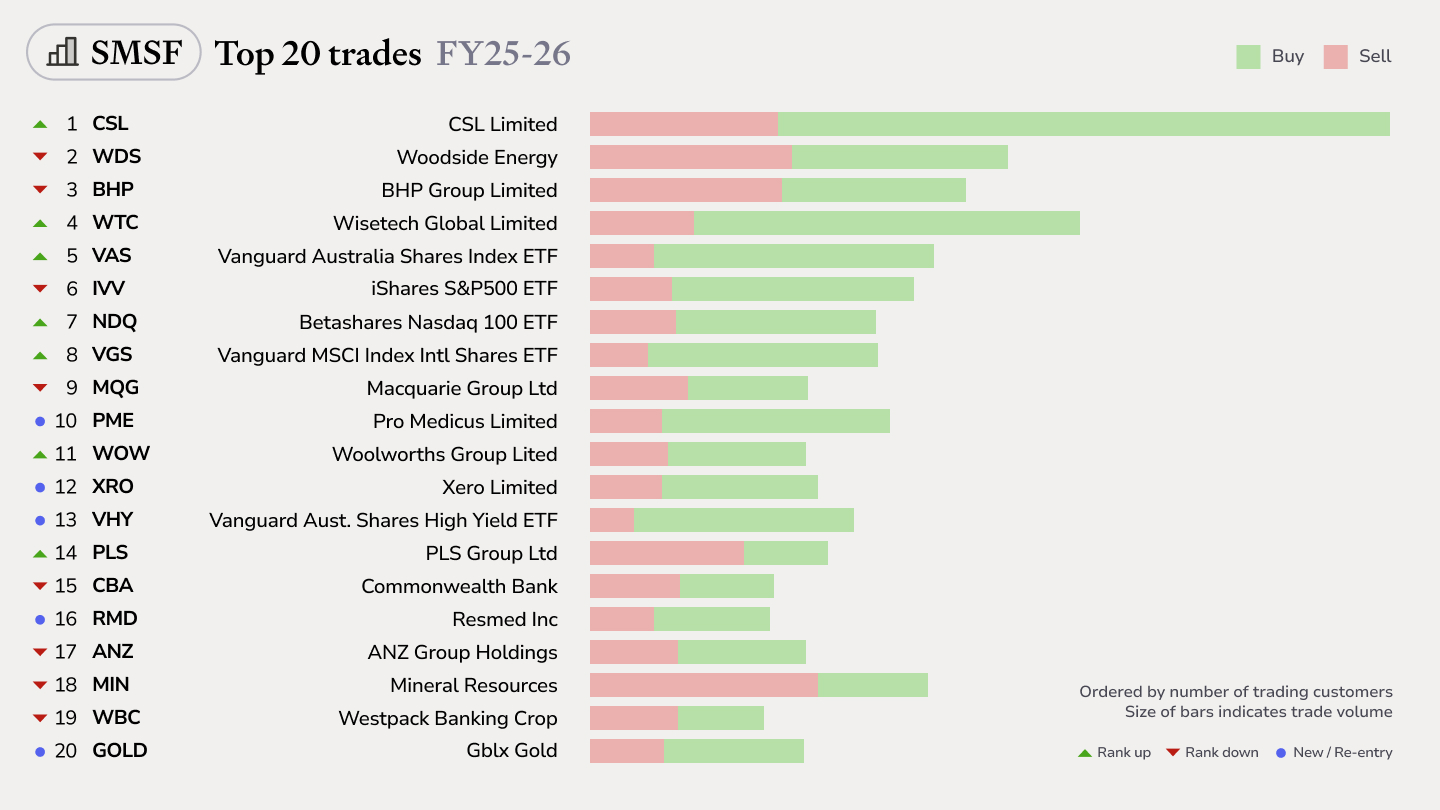

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.