Morningstar analyses Australian investors' top trades of FY26

The 2025-26 financial year was one of shifting expectations. Investors began the year anticipating further interest rate cuts, but persistent inflationary pressures turned that narrative on its head. By year end, the conversation had shifted to whether additional rate hikes are required to bring inflation back to the RBA’s target range of 2-3%.

The ASX200 index was up 2.7% for FY26, modestly below the 10-year annualised return of 5.31% according to S&P data. Technology and healthcare stocks were the biggest drags on performance while materials was a clear standout sector.

Inflation has real consequences for investors. It erodes purchasing power and often leads to higher interest rates. In this environment, investors typically become more selective, risk averse and demand higher returns for riskier assets such as shares.

The start of a new financial year provides an opportunity for investors to reassess their portfolios and determine whether their holdings still align with their long-term investment goals.

Here’s what our Morningstar analysts think about some of the top trades for the 25/26 financial year.

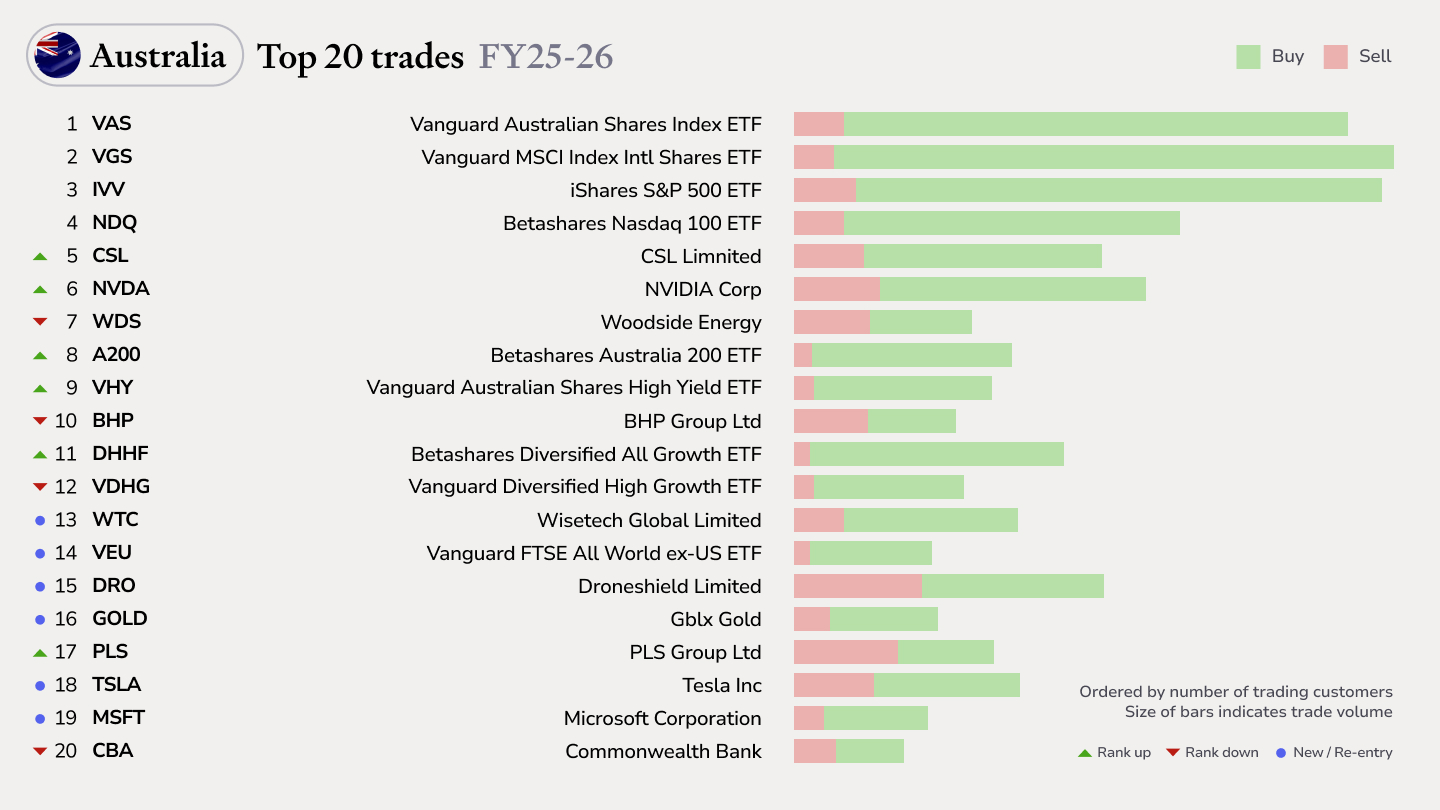

Australian Sharesight users' top trades of the 2025/2026 financial year.

Australian Sharesight users' top trades of the 2025/2026 financial year.

BHP (ASX: BHP)

- Fair Value Estimate: $44 (34% premium at 2/7/26)

- Rating: ★

- Moat: None

BHP has been a recurring top trade for Sharesight users over the years. In FY26, the share price rose 62% on the back of improving commodity prices and strong production from BHP mines. BHP owns several of the world’s largest mines including its copper mine Escondida in Chile and its expansive iron ore mines in the Pilbara region of Western Australia.

While Morningstar believes BHP lacks a moat, it is much rarer to see moats in mining. Mining companies are at the mercy of commodity prices, meaning they will take the price set by the market. Without pricing power, a mining company must exhibit stellar cost efficiencies to justify a moat. Interestingly, BHP’s Pilbara iron ore mines exhibit the low-cost, long-life attributes that would justify a wide moat.

This is partly because the initial investment in developing the mine predates the China economic boom, when development costs were much cheaper. However, BHP’s other mines and operations across the globe do not share the same attributes, which is why we believe it lacks a moat.

A key risk for BHP is its largest customer, China. While China remains a key driving force for current iron ore and copper demand, falling steel production in China is expected to continue. China’s eventual transition to a consumption focused, less commodity intensive economic growth model remains a key headwind for copper & iron ore.

Looking forward, BHP is expected to ramp up iron ore production as well as commence its Jansen potash project in Canada midway through next year. BHP is currently trading above our current fair value of $44 per share. The recent surge in the share price has pushed shares well into the overvalued territory. This has also suppressed the dividend yield to 3.2%, well below the 5-year average of 5.9%. We forecast BHP’s dividend yield for FY27 to be 4.1% (100% franked).

BHP share price performance FY26

BHP share price performance FY26

Nvidia (NASDAQ: NVDA)

- Fair Value Estimate: $280 (30% discount at 2/7/26)

- Rating: ★★★★

- Moat: Wide

Nvidia has retained its spot as one of the most-traded stocks for Sharesight users. Nvidia’s early pioneering in engineering Graphics Processing Units (GPU) have catapulted it front and centre of the AI boom. By combining both software and hardware solutions, Nvidia essentially made themselves irreplaceable for their customers.

Nvidia’s wide moat rating indicates confidence that they can continue to generate excess returns of invested capital over the next 20 years. There are no viable competitors in the current market that could threaten Nvidia’s position. While this can change as technology advances, we believe Nvidia has entrenched itself as the go to market leader.

While Nvidia is seen as the AI beneficiary, its earnings are now heavily influenced by changes in AI spending. We see the biggest risk to Nvidia is cuts to AI capital expenditure from its largest customers such as Google, Meta and Amazon which make up a large chunk of revenue. This risk is a key reason behind its Morningstar Uncertainty Rating of Very High.

While US tech giants are incentivised to build their own inhouse solutions to reduce their spend at Nvidia, high switching costs remain a key concern. The entrenchment of both Nvidia’s software and hardware also increases their pricing power.

Nvidia is currently trading at a sizeable discount to our $280 fair value. This implies there is further upside in valuation, despite the shares rising 30% in FY26. Looking ahead, the key catalysts for Nvidia lie within its Data Centre segment, which is its growth engine. Further development of agentic and physical AI creates a long runway for AI spending in the near to medium term.

NVDA share price performance FY26

NVDA share price performance FY26

Vanguard MSCI International ETF (ASX: VGS)

- Assets Under Management: $16.4 billion (at 2/07/26)

- Rating: Gold

The popularity of ETFs continues to show with the top four trades of FY26 being ASX-listed ETFs. ETFs are easy to access, provide instant diversification and can be used to gain exposure to asset classes generally unavailable to retail investors.

Vanguard MSCI Index International Shares ETF (ASX: VGS) is the second-largest ETF in Australia by assets under management. This ETF mirrors the MSCI World ex Australia Index, which includes the largest international companies across 22 developed markets (exc. Australia) and weights them by market cap. There are currently over 1,200 shares held in this ETF which represents approximately 85% of global shares by market cap in developed markets.

Market weighted indexes naturally adjust to share price movements without frequent rebalancing. Less rebalancing typically leads to lower fees, giving these ETFs an edge in long-term performance.

We believe this specific ETF strategy stands to be among the best choices for global market exposure. The effectiveness of passive management in global markets, cost efficiency and broad diversification are key drivers that earn Morningstar’s Gold rating.

Roughly 28% of the ETF is weighted towards the top 10 largest companies. The top two holdings in the index are Apple (NASDAQ: AAPL) and Nvidia (NASDAQ: NVDA) which make up approximately 10%. While the top end is skewed towards US tech, the vast pool of international holdings creates significant diversification benefits.

The fee is 0.18% per year which places this ETF in the cheapest quintile of the Morningstar Australia Fund Equity World Large Blend Category, where the median fee is 0.85% per year.

VGS share price performance FY26

VGS share price performance FY26

Wrap up

The composition of the Sharesight top trades continues to change year on year. This financial year highlights the growing appetite for both international shares and exchange traded products such as ETFs. While the risk and return profiles between BHP, Nvidia and VGS differ vastly, they represent the larger pool of options available to Aussie investors.

BHP, NVDA & VGS performance FY26

BHP, NVDA & VGS performance FY26

It should be noted that Morningstar’s Fair Value Estimate and star ratings give investors an indicator of the intrinsic value of a share and whether it is over- or under-valued in relation to this value. What these measures do not represent are an investor’s own investment goals and how these companies fit into your portfolio.

Investor goals may range from capital growth, income investing to capital preservation while maintaining purchasing power. Each investment in your portfolio should serve the purpose that your investment strategy is trying to achieve.

Terms used in this article

- Star Rating: Our one- to five-star ratings are guideposts to a broad audience and individuals must consider their own specific investment goals, risk tolerance, and several other factors. A five-star rating means our analysts think the current market price likely represents an excessively pessimistic outlook and that beyond fair risk-adjusted returns are likely over a long timeframe. A one-star rating means our analysts think the market is pricing in an excessively optimistic outlook, limiting upside potential and leaving the investor exposed to capital loss.

- Fair Value: Morningstar’s Fair Value estimate results from a detailed projection of a company’s future cash flows, resulting from our analysts’ independent primary research. Price To Fair Value measures the current market price against estimated Fair Value. If a company’s stock trades at $100 and our analysts believe it is worth $200, the price to fair value ratio would be 0.5. A Price to Fair Value over 1 suggests the share is overvalued.

- Moat Rating: An economic moat is a structural feature that allows a firm to sustain excess profits over a long period. Companies with a narrow moat are those we believe are more likely than not to sustain excess returns for at least a decade. For wide-moat companies, we have high confidence that excess returns will persist for 10 years and are likely to persist at least 20 years. To learn about finding different sources of moat, read this article by Mark LaMonica.

If you would like Morningstar’s insights into your inbox, sign up for the free newsletter.

This article has been prepared by Morningstar Australasia Pty Ltd (AFSL: 240892). The information is general in nature and does not consider the financial situation of any individual. For more information refer to our Financial Services Guide at www.morningstar.com.au/s/fsg.pdf . You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement before making any decision to invest. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser.

Morningstar’s publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Morningstar’s full research reports are the source of any Morningstar Ratings and are available from Morningstar or your adviser. Some material is copyright and published under license from ASX Operations Pty Ltd ACN 004 523 782.

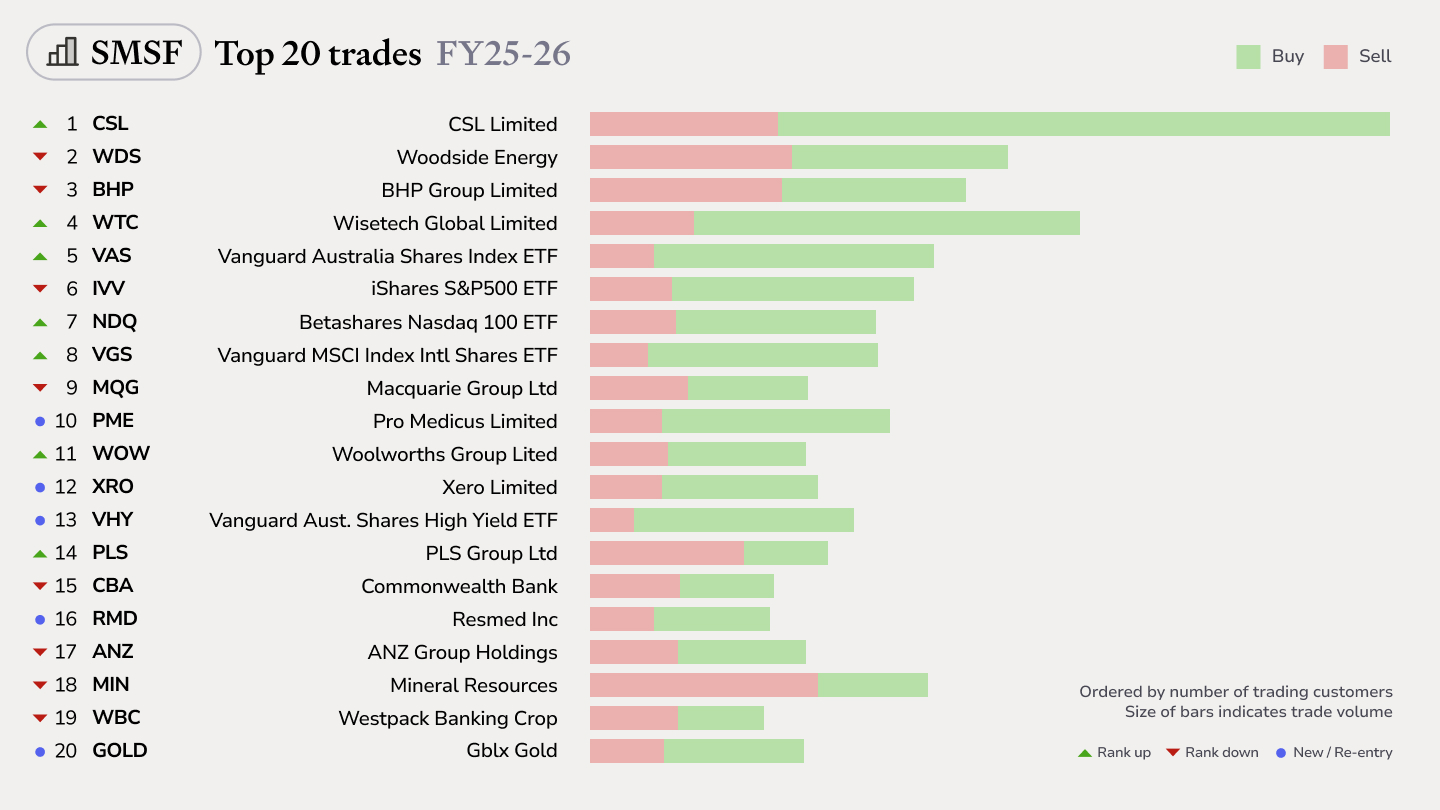

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.

Top trades by Australian Sharesight users in FY25/26

Welcome to the FY25/26 edition of our Australian trading snapshot, where we dive into this financial year’s top trades by Sharesight users.

Sharesight users' top 20 trades – June 2026

Welcome to the June 2026 edition of Sharesight’s monthly trading snapshot, where we look at the top buy and sell trades by Sharesight users over the month.