The time is now for financial planners to embrace fintechs

NOTE: A version of this article first appeared at Adviser Innovation.

Recently the Financial Planning Association of Australia (FPA) released a white paper on fintech titled “Mapping Fintech to the Financial Planning Process - Why Fintech is Not a Threat.”

“Not a threat” meaning fintech provides an opportunity for financial advisors as opposed to eating a financial planner's lunch.

The FPA has done a commendable job assessing the landscape, asking the right questions, and separating out what really should concern financial planners. Disruptive moments are paired with opportunity and they’ve navigated this thoughtfully throughout the report.

Where the fintech ‘threat’ exists

The FPA is an industry body, so it’s natural that they focus on their members: financial planners. What was lacking in my opinion, however, was due focus on the end-client and how financial advisors should respond to a fractured landscape. Plus, there’s a misplaced assumption that people will continue to reliably turn to traditional financial advice in the future.

Sure, money that’s already advised may leak out to fintech challengers, but the bigger, unaddressed threat is technology beginning to capture clients and their assets before they ever become advised in the first place.

I’m the CEO of a fintech, so my opinion is biased, but if you’re a financial planner reading this white paper and learning a bunch of new stuff about technology - you’re in trouble. Certainly in trouble when it comes to new client acquisition and engaging a younger audience.

Those professionals using Sharesight tend to be the most open to using new client-led technologies. With that in mind here are some of our takeaways, taking into account our experience as a fintech:

Why financial planners need to focus on client engagement

The very nature of our solution means that it works best when shared with the end-client, and suits clients needing constructed portfolios of listed securities. In other words, advisors using Sharesight are already off-platform, tend to be independent or family offices, and usually rely on engagement to prove a fee for service model.

The FPA report highlights client engagement throughout:

While process matters, engagement and the connection to the financial planner is a key element to the enhancement of the financial planning process as viewed from the lens of the client. For the fintech industry to present their most significant contribution in the area of engagement uplift presents the financial planner with an exceptional technological opportunity to engage clients.

What strikes us about our advisor partners at Sharesight is their willingness to use a wide spectrum of web-based solutions, especially mainstream, off-the-shelf tech. Put another way: a mobile-first product from Silicon Valley will be better than custom-built dealer-group software (I should know, I used to build custom software for financial advisors!).

The FPA report identified this nicely as well:

The financial planner authorised through a dealer group expects that such technology will come to his or her attention via the dealer group, though dealer groups rarely (if ever) has a fintech manager or lead investigating such technologies.

Operational technology is difficult for small businesses, especially those encumbered by strict regulation. We find that when we’re onboarding a financial advice client, we end up doing a bit of pro bono digital ops and marketing as well.

Fintech products can deliver a better fit for clients

The FPA does a nice job classifying fintechs, and giving examples of how some are deployed. They also acknowledge the dizzying array of new products coming to market. From the FPA:

What is lacking however is an understanding by financial planners, associations, AFSLs and regulators of what is available, how it works and whether or not these solutions actually deliver what they say they do or will.

One thing the report doesn’t address is that once advisors start using these services, fintech solutions will have different levels of staff and client adoption not to mention very different product and service offerings -- this will be a mess operationally.

Think of these like apps on your mobile phone, rather than all-in-one business software. At Sharesight, we know that the portfolios tracked by a certain client only represents a percentage of their total client base.

Product customisation typically won’t be an option either. Many advisors accustomed to the top-down model of enterprise software deployment are in for a surprise. Those leveraging fintech successfully will understand that fintechs solve 98% of a hyper-specific problem really well, and will bring themselves to ignore the remaining 2%.

Additionally, most fintechs operate at scale, some globally. Some may send staff to an advisor’s office for in-person training, others may respond via Twitter. These service models will take some getting used to. That’s not to say fintechs don’t provide quality client service, but it’s worth keeping the price tag in mind when expecting a face-to-face meeting with a sales rep.

Getting a second opinion aka “Hey Google, what are the best investments?”

While the FPA report covered client engagement well, they didn’t cover trends within the self-directed market (we note this was an FPA report). To be a successful financial advisor in the fintech age is to acknowledge what happens outside of their purview or when a prospective client leave their office.

People Google everything and spend hours each day on social media apps. This means they’ll be targeted by a range of products by virtue of their browsing history (Spaceship super, anyone?)

Plus, the experiences we have online these days are so much better than what traditional financial services offer. Try comparing booking a holiday on Airbnb with checking your super balance. Fintechs are exploiting this. The FPA (actually Matt Heine from Netwealth) did a nice job acknowledging something we’ve been saying:

There needs to be due attention paid by the financial planning profession. Clients are not comparing the services of a financial planner any longer to banks and institutions. Rather they are starting to compare all services to the information flow that is timely and relevant from Amazon, Facebook and Google. They engage with Uber, Menulog, Netflix, Virgin Active, the weather, Qantas, Red Energy, the Post Office, myGOV, Medibank, Opal, and just about every aspect of day to day life via technology including apps.

What happens if these Fintechs, you know, talk to each other?

The FPA report identified fintech challengers in isolation, with each corresponding to a specific part of the advice chain. While that was mostly true, a trend we’re seeing - and helping to propagate - is increasing connectivity between challenger solutions.

We often hear incumbents talking about how fintech X or Y wants to put them out of business or take over a major share of someone’s “wallet.” In reality, fintechs are run by ex-financial services people hell-bent on fixing a specific problem. Since they’re operating at scale, they don’t care about things outside of a very narrow lens.

How financial planners can win with fintech

Advisors need to get digital fast. Their websites need to evolve from what amounts to a brochure into an engaging experience that captures prospects’ details. Advisors will also need to embrace a gradation of services. Some clients will still want to delegate everything, some will want more control. Advisor fee models will need to adapt to this.

Overnight disruption in financial services is an illusion, but advisors will see fewer clients and asset flows as the industry comes under more pressure from all sides. Rather than viewing fintechs as a threat to their business, financial planners should take the time to examine the opportunity that they can bring. The time is now for financial planners to embrace fintechs.

FURTHER READING

Save time and money by sharing your portfolio with your accountant

It's easy to save time and money at tax time by sharing access to your Sharesight portfolio with your accountant. Keep reading to learn more.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

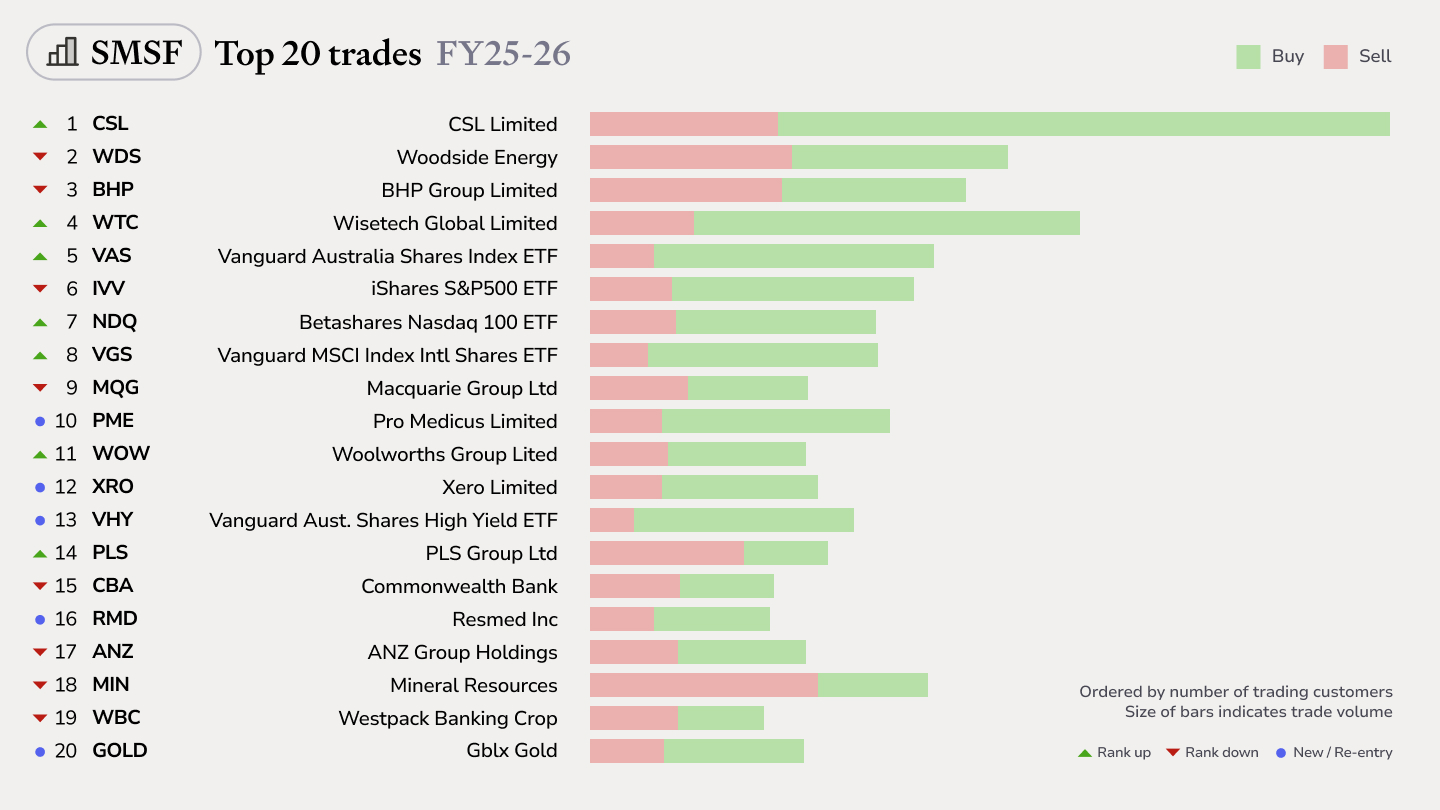

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.