Wrap-up of the 2017 British Australian Fintech Forum

Last month Sharesight was invited by the Australian British Chamber of Commerce to represent Australian fintech on a trip to London.

This was a terrific experience. In addition to planning our expansion into the UK, this trip served as an eye opener as to how far ahead the UK is regarding tech-friendly financial regulation.

Open Data

First and foremost UK banks are well down the track of the Open Banking initiative, which mandates that all banks give customers (and fintechs) access to their data through a common set of APIs. Some of the work is already complete, with the ultimate deadline in 2018.

If bank data and APIs bore you, just know this obliterates one of the most important barriers to competition in financial services. If you’ve struggled to set up a portfolio on Sharesight, this regulation would make that process super easy. The end result would function like our Broker Import feature, but for all investment accounts from all institutions -- shares, cash, super, platform products, etc.

These APIs will power the Sharesight UK solution, and we can’t wait to get started.

@sharesight Doug creating value for users, investors and rebel alliance (fintech wealth space) #BAFF2017 pic.twitter.com/2SZiqc3wTO

— Katherine Heathcote (@KatieHeath23) April 21, 2017

Fintech-friendly regulation

The UK (especially the city of London) understands how important financial services are to the economy and they’ve fully embraced financial technology. Because of London’s diversity and talent pool, its location, and because they take a global outlook from day one, they have a distinct advantage over every other city in the world including New York and San Francisco. Brexit only seems to add to their sense of urgency in terms of extending their lead in fintech-friendly regulation and taxation.

Some of the investor and startup friendly regulations include:

- 25% research and development tax credit.

- EIS (Enterprise Investment Scheme): 30% tax credit for individual investors, no capital gains tax after 3 years of ownership, and generous loss relief, up to nearly 100% of the initial investment.

- SEIS (Seed Enterprise Investment Scheme): similar to the above but with 50% tax credit, plus capital gains reinvestment relief.

- A planned 17% corporate tax rate.

- Robust FCA (Financial Conduct Authority) sandbox with 70+ current participants.

London’s crowdfunding market is mainstream enough to support mass market ad campaigns -- the Tube is plastered with equity crowdfunding ads touting the latest campaigns.

The UK now has two fully operational startup banks providing a legitimate alternative to traditional high street brick and mortar branches. One, Starling Bank, got up and running within a year. This demonstrates the robustness of the UK fintech market.

Aussie fintechs

The nine companies on the trade delegation represented Australia exceptionally well. Although Australia is a more challenging market from which to build a startup, these constraints have arguably made us scrappier and more creative. I didn’t see any discernible talent gap between UK and Australian fintechs.

Sharesight was joined by:

- Ed Jones, Neu Capital

- Rob Lincolne, Paydock

- Charlotte Petris, Timelio

- Jack Stevens, Edstart

- Emma Weston, AgriDigital

- Chris King, Splend

- David Jordan, Solutions4Strategy

- David Price, Mafematica

We were also joined by Toby Heap, Founding Partner of H2 Ventures and Non Executive Director of Stone & Chalk and Andrew Corbett Jones, Head of the Tyro Fintech Hub. Both provided terrific insights and helped spur discussions at all the events.

FURTHER READING

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

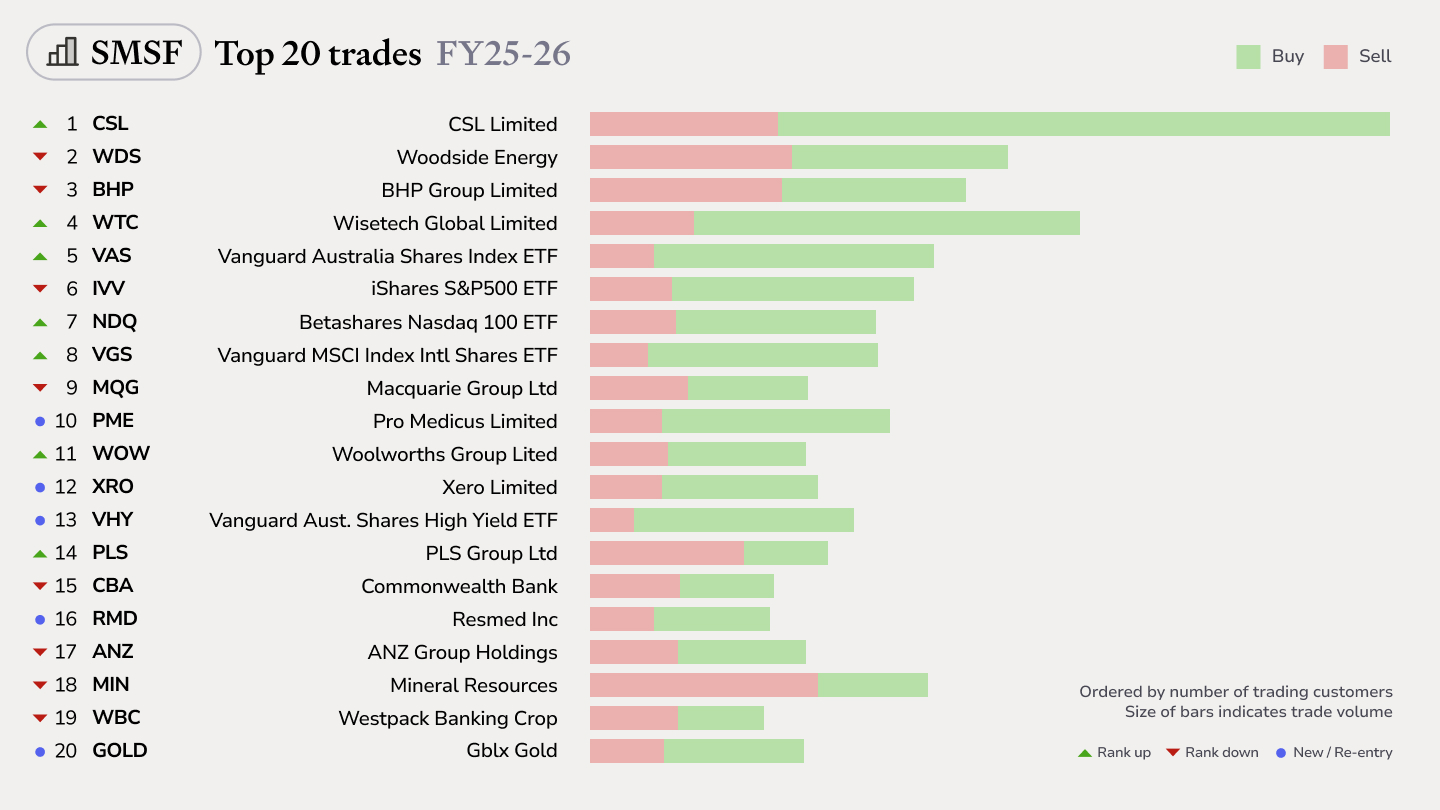

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.

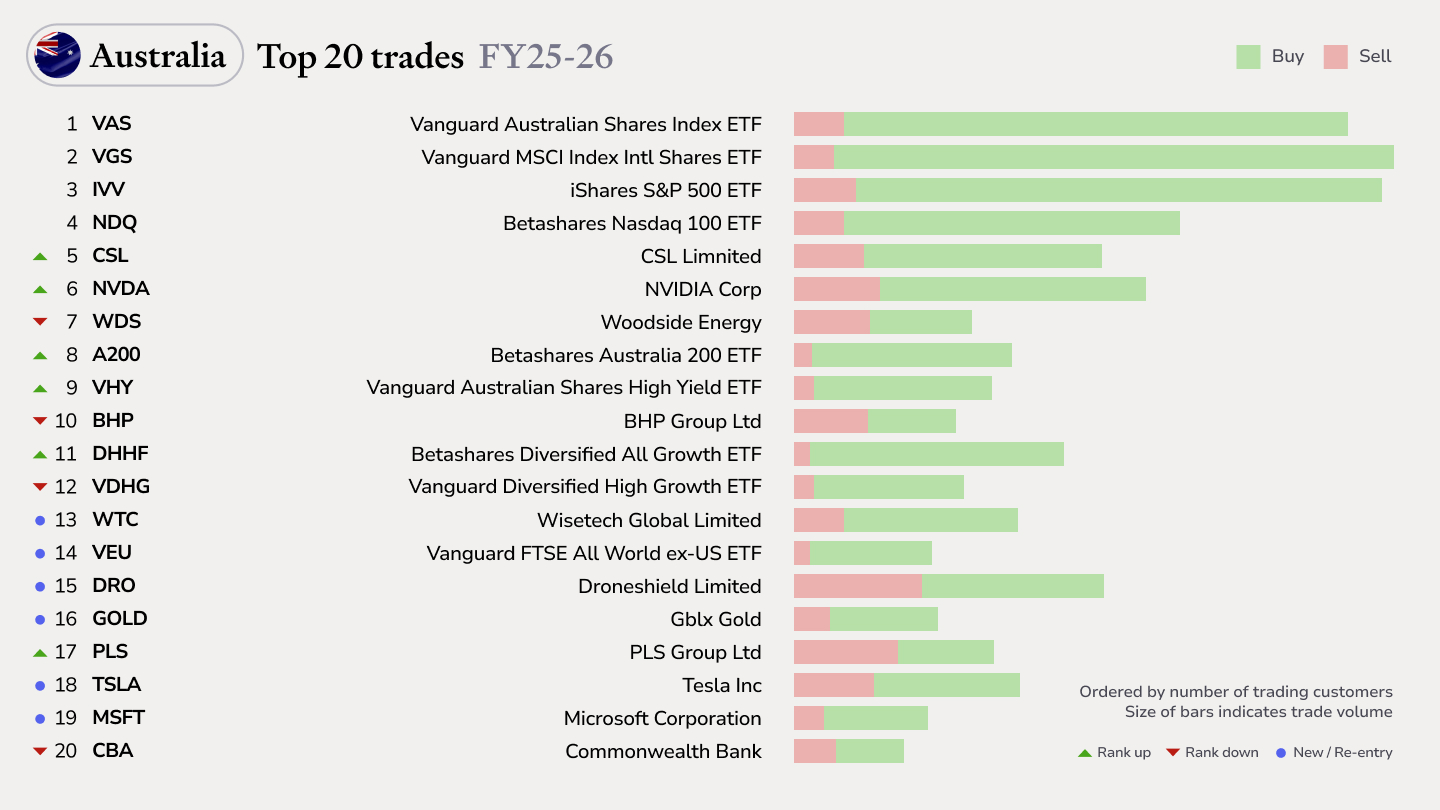

Top trades by Australian Sharesight users in FY25/26

Welcome to the FY25/26 edition of our Australian trading snapshot, where we dive into this financial year’s top trades by Sharesight users.