How SMSFs can save money using Sharesight

Disclaimer: This article is for informational purposes only and does not constitute a product recommendation, taxation or financial advice and should not be relied upon as such. Please check with your advisor or accountant before using Sharesight or any other tool for your SMSF, to ensure you meet the ATO’s compliance obligations

Investors are taking control of their finances by establishing self-managed superannuation funds (SMSFs) as well as cutting ties with traditional platforms and WRAPs — increasingly playing an active role in the investment decisions that impact their retirement. All of this has been propelled by the rapid expansion of consumer facing financial technology.

As investors seek to cut costs by moving away from full service platforms and providers, they need to assemble their own suite of tools to manage their investments, in a process known as ‘unbundling’. In this article we’ll explore a number of different bundled and unbundled solutions, and compare the benefits and costs of each.

What is unbundling?

Unbundling refers to the process of moving away from these monolithic, expensive, vertically integrated financial products and building your own "unbundled" solution — connecting products from across the fintech ecosystem to achieve the same outcomes — usually for a fraction of the cost.

There was a time that it made financial sense to bundle all of our financial service products together with a single institution, i.e. buying our insurance from the same bank we hold our home loan with, who we’ve also held a savings account with for most of our lives. But with the proliferation of fintech platforms like Sharesight that make it easy to import your investment data, you’re no longer constrained by the need to centralise this data with one financial institution.

5 problems SMSF trustees need to solve

There are five ‘problems’ an unbundled SMSF solution needs to solve:

-

Execution: The actual buy/sell transactions of investing.

-

Accounting: Ensuring your SMSF meets compliance requirements of Australian SMSF legislation.

-

Compliance: Making sure that the SMSF follows the ATO requirements.

-

Research/Advice: Choosing shares, funds, or other investments based on your investment strategy (the part you will probably spend the most time on if you unbundle).

-

Portfolio tracking: Tracking how your SMSF portfolio is performing against your investment strategy.

An SMSF trustee can take more control of their portfolio (and reduce costs) by using off-the-shelf platforms for many of these pieces.

Three potential approaches to running an SMSF

For our analysis, we’ve constructed three approaches to running an SMSF. These aren’t the only approaches and this is what makes the ‘unbundled’ approach so powerful, as investors can mix and match components to suit their requirements.

Our example SMSF approaches

1) Full service SMSF — Offloading most of the administration and decision making to full service WRAP platforms, accountants and financial advisors, these often attract fees based on the value of the funds under management (FUM) of the SMSF portfolio.

2) Low cost SMSF with financial advice — For investors who want to be more hands-on with their SMSF but want to consult with a financial advisor on strategy and investment decisions, this offers a mid-point, though with the financial advisor charging based on FUM, costs in this scenario will increase over time as the portfolio grows.

3) Low cost SMSF DIY — For the fully hands-on investor, who wants to spend time actively looking for investment opportunities, conducting their own research (with a subscription to a financial research publication), and tracking their SMSF portfolio with Sharesight, this offers a relatively fixed cost regardless of the portfolio size, which decreases the impact of costs on the portfolio return as it grows over time.

SMSF administration cost breakdown

Let’s look at the costs to manage a typical $500,000 SMSF portfolio using our three scenarios:

| Full service SMSF | Low cost SMSF with advice | Low cost SMSF DIY | |

| Execution | SMSF WRAP platform

Cost: 0.86% FUM |

Low cost broker

Cost: $95/y (10 trades) |

Low cost broker

Cost: $95/y (10 trades) |

| Accounting | Accountant

Cost: $2,750/y |

Accountant that uses Sharesight

Cost: $2,000/y (lower costs as there’s less to do at year end) |

Accountant that uses Sharesight

Cost: $2,000/y (lower costs as there’s less to do at year end) |

| Compliance | Accountant or tax professional

Cost: 0.5% FUM |

SMSF compliance platform

Cost: $200/y |

SMSF compliance platform

Cost: $200/y |

| Research/Advice | SMSF WRAP platform

Cost: Bundled with execution/admin fees |

Financial advisor

Cost: 0.5% FUM |

Online premium research subscription

Cost: $2,000/y |

| Portfolio Tracking | Financial advisor

Cost: Bundled with compliance fees |

Sharesight (Expert)

Cost: $588/y |

Sharesight (Expert)

Cost: $588/y |

| TOTAL ANNUAL COST* | $9,550 | $5,383 | $4,882 |

*These fees were sourced from the most recent PDS available for the platforms we reviewed when writing this article. Please refer to the PDS of your platform(s) for information specific to your scenario. All prices in AUD.

SMSF cost scenario notes:

-

In scenario 2/3, because the investor is offloading much of the administration burden from their accountant by keeping their portfolio up to date in Sharesight, this minimises accounting costs at the end of the year.

-

In scenario 3, the investor could save even more by forgoing an online research subscription, instead relying on publicly available company information and finance websites — this would bring the cost down to only $2,726/year.

-

Because of the FUM component, the impact on returns from scenario 1/2 increases over time,** dramatically impacting long term returns **(which is significant over the typical lifespan of an SMSF portfolio).

Track your SMSF portfolio performance with Sharesight

Join over 200,000 investors tracking their investments with Sharesight by signing up today. Built for the needs of SMSF trustees, with Sharesight you can:

-

Organise holdings according to your documented SMSF asset allocation and investment strategy, providing valuable insights throughout the year.

-

Easily share SMSF portfolios with accountants or financial professionals to make admin and tax compliance a breeze.

-

Track SMSF investment performance with prices, dividends and currency fluctuations updated automatically.

-

Run powerful tax reports built for Australian investors, including capital gains tax, unrealised capital gains, and taxable income (dividend income).

Sign up for a free Sharesight account to get started tracking your SMSF portfolio performance today.

FURTHER READING

Save time and money by sharing your portfolio with your accountant

It's easy to save time and money at tax time by sharing access to your Sharesight portfolio with your accountant. Keep reading to learn more.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

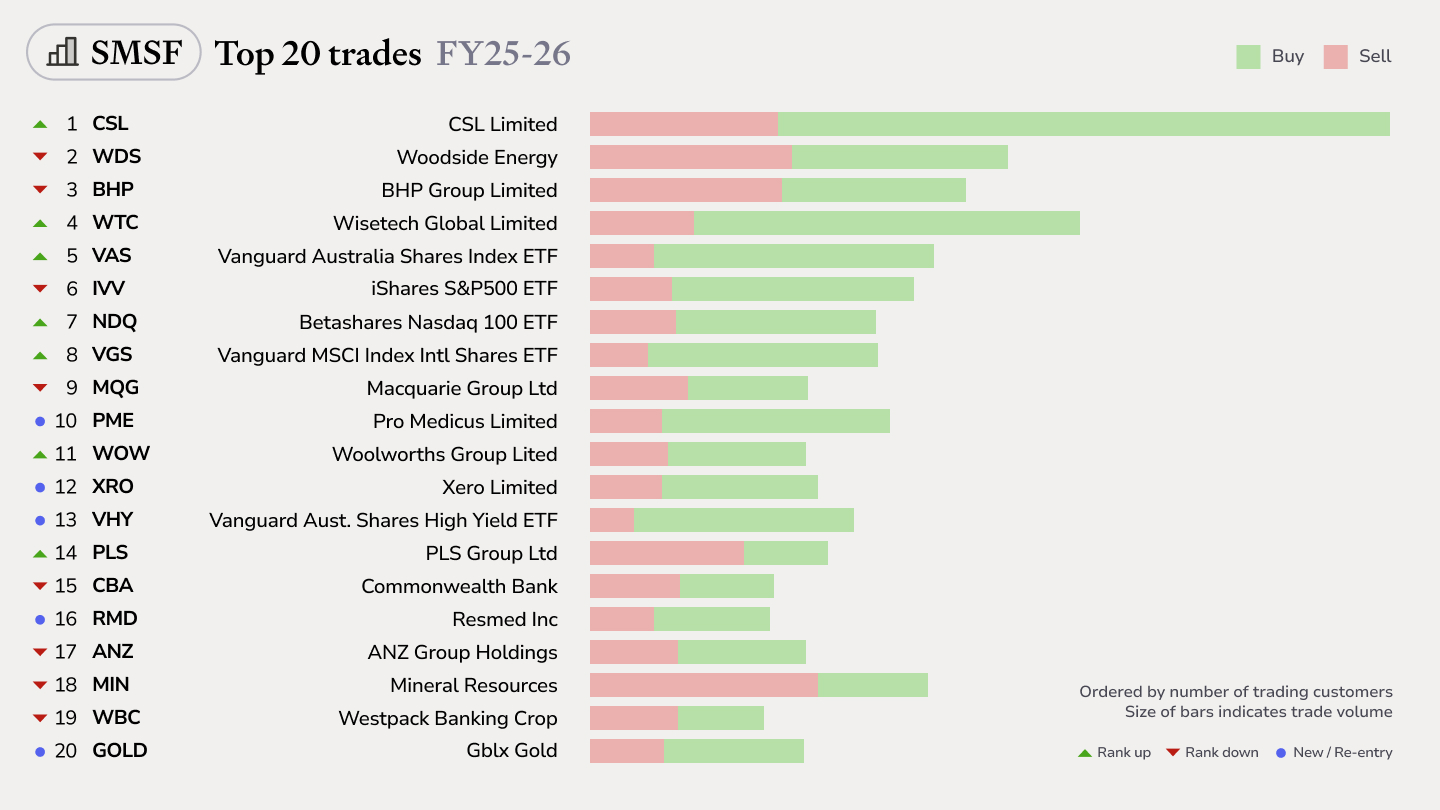

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.