Mutual Funds vs. ETFs in Canada

Disclaimer: The below article is for informational purposes only and does not constitute a product recommendation, or taxation or financial advice and should not be relied upon as such. Please check with your adviser or accountant to obtain the correct advice for your situation.

Mutual funds and ETFs are often seen as similar investment vehicles, as both make it easy to invest in a basket of underlying assets. But there are important differences between the two, particularly when it comes down to cost, tax treatment and how investors buy and sell each.

In this blog we’ll explore how mutual funds and ETFs differ, and what you need to look out for if you’re a Canadian looking to invest.

Mutual funds

Mutual funds are pooled investment products managed by professional fund managers. They offer investors access to a diversified collection of stocks, bonds and more exotic underlying investments such as real estate holdings across a range of sectors and markets in a single fund. Because the fund size is far greater than the contribution of any one investor, mutual funds offer scale, diversity, reduced risk and less exposure to market volatility than investing in a single company or industry would.

In a Canadian context, mutual funds have been described as "culturally entrenched as hockey, housing and snow" due to their long track record as the investment vehicle of choice. This message to investors has been clear and reinforced by banks and financial institutions for over thirty years: mutual funds are seen as a key component of any strategy to build wealth or save for retirement.

ETFs

Like mutual funds, ETFs are a pooled investment product offering investors access to a diversified collection of stocks and other securities like bonds. Traditionally, ETFs were designed to track an index, commodity or currency, allowing investors the diversification of a mutual fund with the trading characteristics of a security that can be bought or sold on a stock exchange.

While ETFs first came to prominence as passive, index-tracking products, the last few years have seen a great deal of interest in actively managed funds. At the start of 2020 there were 905 listed ETFs in Canada with 377 or 41.7 percent of these being actively managed ETFs. ETFs also steadily increased their share of total investment fund assets from 7.3% in mid 2016 to 11.2% by 2020.

Trends in Canadian ETFs & mutual funds

Most Canadians still prefer to invest in mutual funds due to their long track record in the North American market but investors are increasingly being drawn to the flexibility of Canadian-listed ETFs. Data from the Investment Funds Institute of Canada (IFIC) put total Canadian mutual fund assets under management at $1.6 trillion at the end of 2019 while ETF assets under management came in at $205 billion. However, ETFs enjoyed a stellar 2019 with about $30 billion in asset growth and plenty of momentum: almost half of these inflows arrived in the final three months of the year, the sector’s best quarter on record.

Mutual fund & ETF costs in Canada

Mutual funds are typically more complex products than ETFs and this often translates into higher management fees. Generally, the annual cost breakdown will include an overhead or admin fee, fund manager charges and trailing commission to the financial advisor or firm that sold the fund to the investor. According to a report issued by Morningstar in 2019, Canada has some of the highest expense ratios for mutual funds in the world. This is largely due to funds usually being sold by a financial advisor working for one of Canada’s major banks.

On the other hand, ETFs are generally seen as a low-cost way to earn a return similar to the index, commodity or currency being tracked. They can also be bought the same way you buy and sell shares but far more cheaply than investing directly in multiple listed companies. Management fees are lower, even for more active ETFs, as competition amongst providers is fierce, there is no embedded commission to be paid and servicing costs are well below those of mutual funds.

While lower annual fees and no minimum investment barrier might make a strong case for ETFs to price-sensitive investors, there are three points to consider.

-

Firstly, mutual fund investors pay higher fees for the services of a professional fund manager with an established record of investment selection and portfolio management.

-

Secondly, ETF investors who trade frequently may incur an extra cost. It is worth reviewing the major Canadian bank and non-bank brokerage houses currently trading in ETFs to get an idea of the price structures of each provider.

-

And finally, most mutual funds are sold as part of a broader financial advice process, making direct cost comparisons with ETFs acquired via a broker difficult.

Buying and profiting

Mutual funds in Canada are usually purchased via a financial advisor or directly from a mutual fund company – in both cases likely to be the subsidiary of one of the major banks. ETFs can be bought directly via a broker. In both cases it is prudent to do your homework and shop around before deciding. Performance, cost/commission and minimum purchase amount are all factors that should be taken into account.

With both ETFs and mutual funds investors can potentially profit in two ways. The first is the capital gain when selling out of a fund for more than you paid for it. The second is with distributions in the form of dividends, interest, capital gains or other income the fund earns on its investments. A mutual fund offers investors the option of receiving distributions in cash or, more typically, having them reinvested in the fund. ETFs don’t reinvest cash distributions in more units or shares but rather hold this cash in the investor’s account until instructed on how it should be invested.

ETFs, Mutual Funds… or both?

Canadian ETF investors tend to enjoy the responsibility of managing their investments and value transparency. This "hands-on" component is important as ETFs trade like stocks and their price fluctuates over the course of a day. As well as the ability to trade whenever the market is open, ETF investors can apply a range of traditional stock strategies such as placing stop-loss or limit orders and short selling.

Mutual funds tend to suit more traditional "mom and dad" investors who want a simpler product and are happy to pay a premium to see their portfolio professionally managed. These investors may also be after some of the more complex features of mutual funds that aren’t available in ETFs, such as a regular cashflow or more tax efficient outcomes. Unlike ETFs, mutual funds are only priced at the end of each trading day when the net asset value is updated.

Those seeing the merits in both products should also consider actively managed ETFs as these capture many of the similarities between the ETF sector and more traditionally managed products. In both cases a fund manager is engaged to make the investment decisions, although the active ETF aims to outperform a benchmark index while a mutual fund manager may have a far broader remit to spot market irregularities to the benefit of investors. This line may become increasingly blurred in the future as the ETF industry continues to grow in complexity and seeks greater diversity in both products and investment strategies

Track Canadian ETFs and Mutual Funds with Sharesight

Sharesight’s portfolio tracker makes it easy for Canadian investors to keep track of all their investments in one place, with the ability to track over 12,000 Canadian mutual funds plus thousands of other Canadian and global ETFs and stocks.

It’s simple to add Canadian mutual fund or ETF trades to your portfolio:

-

Sign up for a FREE Sharesight account.

-

Add your holdings to your portfolio(s) by searching for the ETF by its stock code in the relevant market, or the mutual fund’s name in the FundCA market. You can also use the Sharesight File Importer to bulk import trades to your portfolio.

-

Sharesight converts the prices and valuations of your holdings from their listed market to your portfolio’s base currency. It also automatically calculates any currency fluctuations on a daily basis and backfills past distributions (and continues to add new ones as they are announced).

Start tracking Canadian mutual funds and ETFs with Sharesight

If you’re not already using Sharesight to track your investments, what are you waiting for? It’s free to sign up, and with Sharesight you can:

-

Track all your investments in one place, including stocks, mutual/managed funds, property, and even cryptocurrency

-

Get the true picture of your investment performance, including the impact of brokerage fees, distributions, and capital gains with Sharesight’s annualised performance calculation methodology

-

Run powerful reports built for investors, including Performance, Capital Gains Tax (Australia and Canada), Portfolio Diversity, Contribution Analysis and Future Income (upcoming distributions)

-

Easily share access to your portfolio with family members, your accountant or other financial professionals so they can see the same picture of your investments that you do.

Sign up for a FREE Sharesight account and get started tracking your investment performance (and tax) today.

FURTHER READING

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

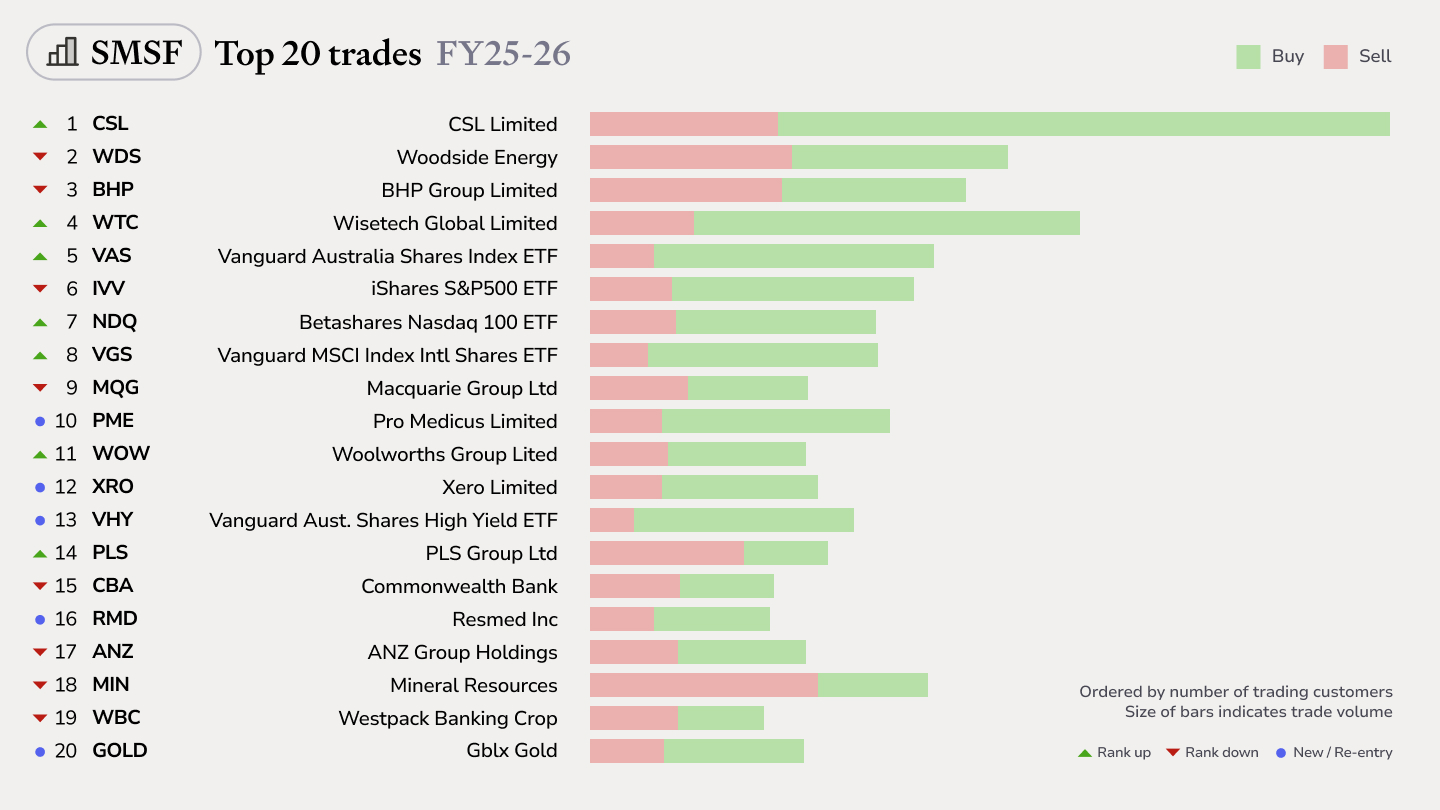

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.

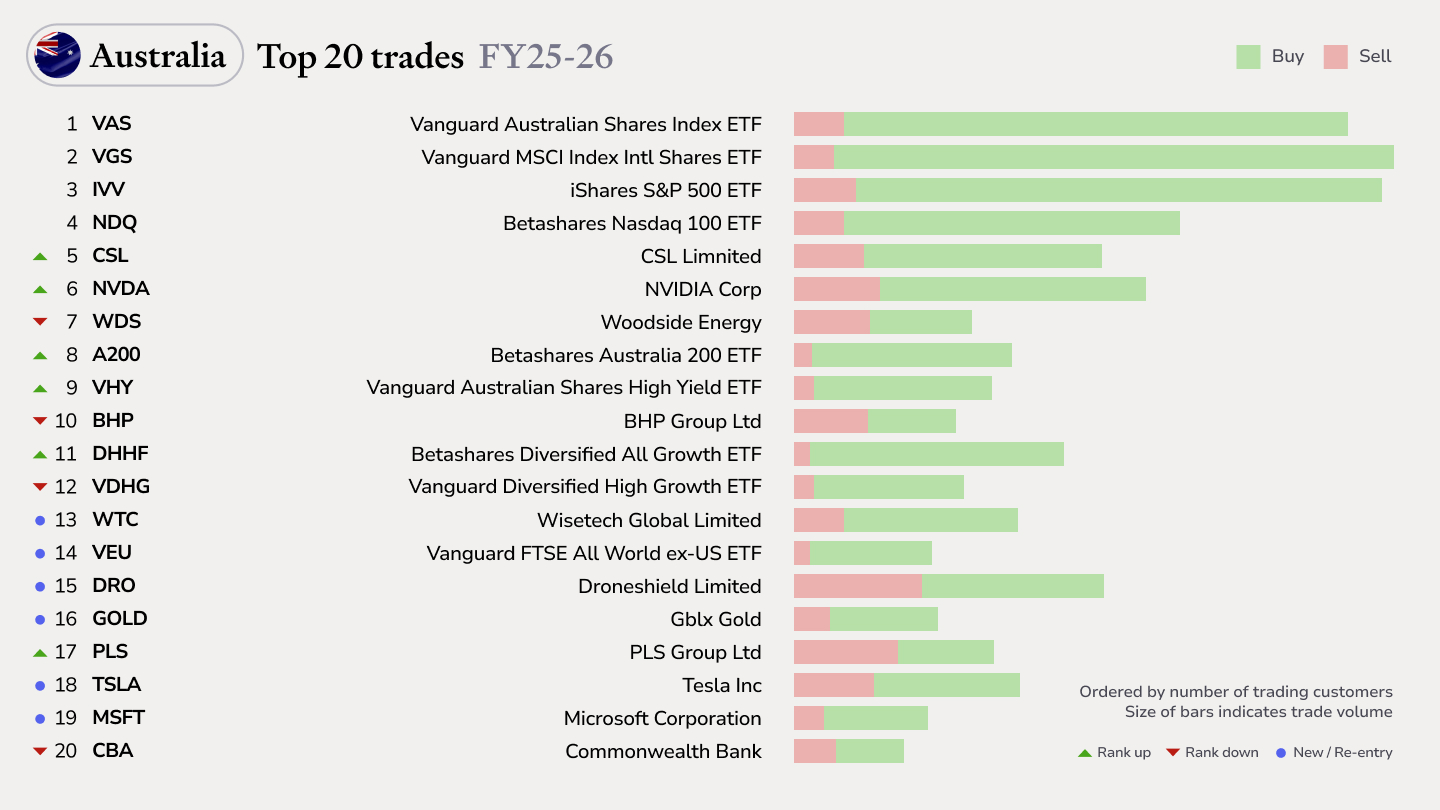

Top trades by Australian Sharesight users in FY25/26

Welcome to the FY25/26 edition of our Australian trading snapshot, where we dive into this financial year’s top trades by Sharesight users.