What is unbundling and how much can it save me?

If you subscribe to the financial industry trade press or keep an eye on Australian SMSF news you've probably come across the term "unbundling." Unbundling refers to the surgical destruction of vertically integrated products and services that have been pushed by the big banks for decades. It's very real. And it's very possible to do.

A bundled offering used to make sense. Before our "life admin" could be run across tabs in a browser, it made sense to buy our investments and insurance from the same place we got a home loan and did our everyday banking. Lower cost options probably existed, but the time and effort required to research them and fill out the paperwork required to switch wasn't worth it.

Fortunately, we live in the age of the informed consumer. "Ticket clippers" waiting in the middle to take their pound of flesh are disappearing or having to adapt to provide something of value.

Let's take an investor with a $500,000 portfolio and see how the costs compare.

The unbundled solution

1. Execution — CMC Markets

Their entry level service starts at $11 per trade and gets cheaper the more you execute. But, let's assume that 30% of the portfolio turns over annually, charged at 20 basis points. That's $300 in trading fees annually. We should also assume that in addition to shares, our investor is using ETFs, which would incur fees of their own. Let's say half the portfolio is invested in ETFs, which have a management fee of 0.3%. That's $750 annually (ETF fees range from 0.2% to 0.6%).

2. Accounting — Xero

Our investor has wisely chosen to use an accounting application. Not only will this force him to be more organised, it should reduce his accounting fees at tax time. Xero Cashbook is around $15 per month, or $180 per annum (the accountant will likely bundle this cost into the overall fee). He'll also need to pay his accountant for their services. This might run $1,000 assuming a decently complex financial situation.

3. Research — Intelligent Investor

Always wise to get independent advice. In addition to company research, Intelligent Investor provides model portfolios and access to analysts in their Unlimited Share Advisor package for $64 per month, or $768 per annum.

4. Portfolio Tracking — Sharesight

While understanding his portfolio tax liability is a must-do, knowing exactly where his portfolio is in terms of capital gains, dividends, and currency is just plain smart. And like using Xero, this should reduce accounting or bookkeeping costs. The Sharesight Standard plan is $25 per month, or $275 for an annual subscription.

5. Cloud Apps — Google

It might seem like Google doesn't belong on this list, but opening a dedicated Google account for all-things-investing makes sense. Not only can our investor maintain a dedicated email account, but he can keep organised using their suite of apps: calendar, docs, spreadsheets, sites, and storage (Drive). All info can be shared with a spouse, and accountant, and so forth. And it's free! Annual cost: $0. Honestly, the free Google services are better than their relatively expensive Microsoft antecedents (Office).

The unbundled bottom line: $3,093 per annum

Plus, via Sharesight, 3 of the above service providers talk to each other, meaning admin work is seriously diminished. A trade made with CMC will flow to Sharesight, which appears in Xero. In real time. While our investor sits on the beach with a cold beer in hand.

The traditional bundle

Bundled solutions charge based on assets under management. Staying with our $500,000 example:

Execution, Research, Advice, and Portfolio Tracking — Investment Platform or Wrap Account

The selling point of platforms and wraps is that they do the above three things for you, but that comes at a cost:

- Typically, you'll need to pay between 1.5% and 2% in annual fees for administration (that's the piece Sharesight does for $275).

- Then there's the adviser fee. You can't get money onto a platform without "hiring" an adviser. They usually take another 1% to 2%.

- Then there are the fees paid to the managers of the actual investment products, which sit on the platform. These run between 0.75% and 1.5%.

- Last there are miscellaneous one-off fees, like entry and establishment fees.

That totals between 3.25% and 5.5%. Most industry sources peg the cost of using bundled solutions between 3% and 5% annually. Conservatively, let's stick with 3%.

The bundled bottom line: $15,000 per annum

And we haven't even paid for the accounting yet! You have no control or visibility over your data and any performance or tax report will be mailed to you in a print-out that looks like it was generated on a dot-matrix printer.

Even if a fee of 3% annually sounds palatable, when you think about this in terms of ROI (alpha) it looks a lot worse. Assuming returns of 8% per year, a 3% fixed fee soaks up nearly 40% of your return!

Do you have to sacrifice professional advice if you unbundle?

No. It's worth noting that the unbundled scenario above does not include financial advice. Fortunately, there are new low-cost or fixed-fee options springing up. Given the money saved by unbundling, even experienced investors might allocate a portion of their assets to these new options. It could be worth the time savings alone.

Stockspot, for example, will allocate money to a basket of ETFs and take care of the rebalancing for you. They charge 1.2% per annum + a $77 admin fee. If our investor allocated 20% of his portfolio to Stockspot that would be $1,317 per annum. Combined with the unbundled fees, that would still be far below $15k.

Unbundling is great for those who know what they're doing, but it's not for everyone. Many, many people benefit greatly from sound financial advice. A well-intentioned, fee-for-service financial adviser will investigate options on your behalf both on and off platforms and wraps.

It's a shame that the pricing disparity illustrated above is so great. It means that people who don't know what they don't know are getting a raw deal.

This information is not a recommendation nor a statement of opinion. You should consult an independent financial adviser before making any decisions with respect to your shares in relation to the information that is presented in this article.

FURTHER READING

Save time and money by sharing your portfolio with your accountant

It's easy to save time and money at tax time by sharing access to your Sharesight portfolio with your accountant. Keep reading to learn more.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

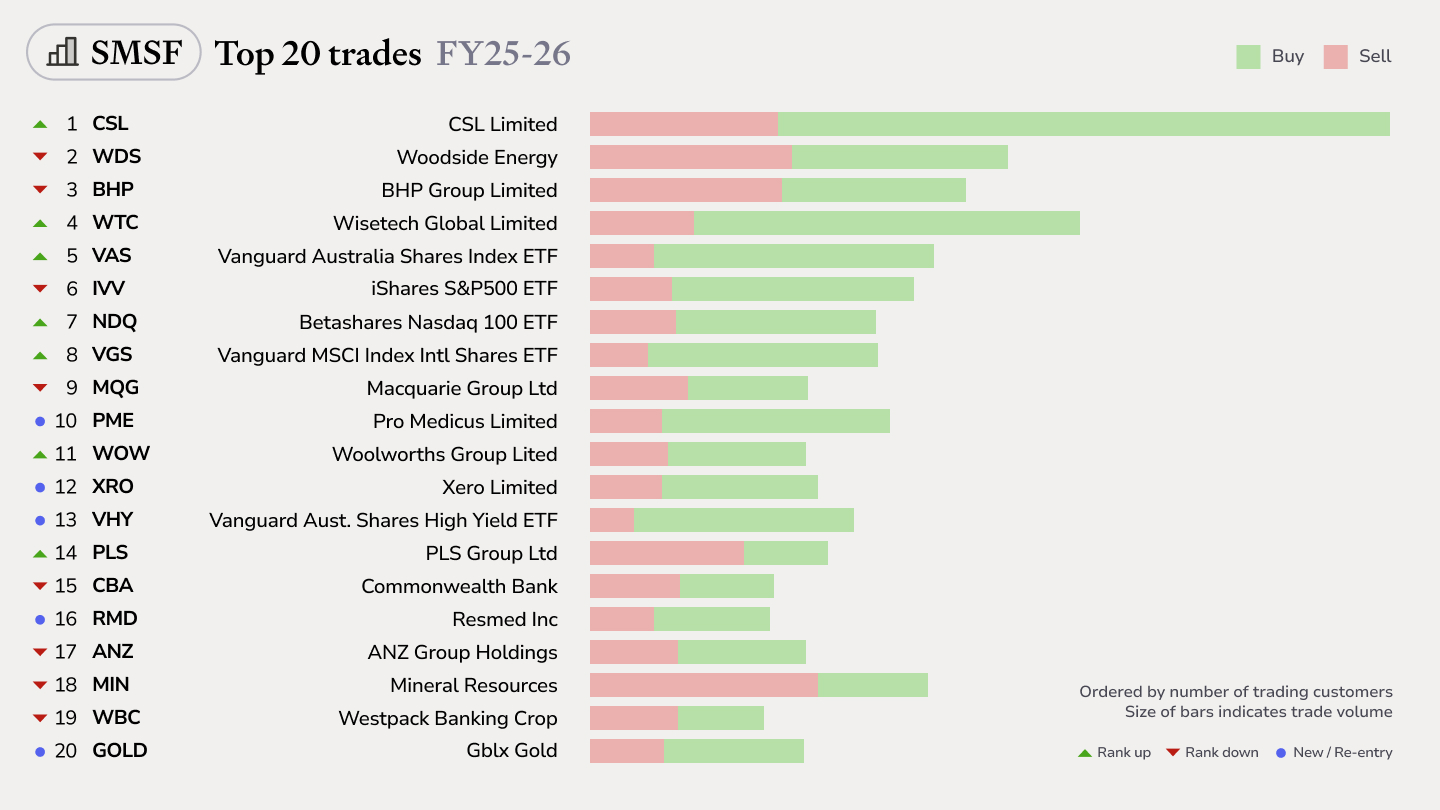

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.