Morningstar's 2022 Individual Investor Conference: Key takeaways

Disclaimer: This article is for informational purposes only and does not constitute a specific product recommendation, or taxation or financial advice and should not be relied upon as such. While we use reasonable endeavours to keep the information up-to-date, we make no representation that any information is accurate or up-to-date. If you choose to make use of the content in this article, you do so at your own risk. To the extent permitted by law, we do not assume any responsibility or liability arising from or connected with your use or reliance on the content on our site. Please check with your adviser or accountant to obtain the correct advice for your situation.

We recently had the pleasure of exhibiting at Morningstar’s 2022 Investment Conference for Individual Investors, where investors had the opportunity to hear from industry experts and discover leading solutions to help them achieve investing success.

It was great to meet so many passionate investors and have the chance to showcase our partnership with Morningstar, which brings together leading research and data with advanced performance and tax reporting tools, helping investors streamline their portfolio tracking, analysis and reporting.

Our ‘lunch and learn’ session, hosted by Sharesight CEO Doug Morris and Morningstar’s Head of Product Management, Mark LaMonica.

Meeting investors and giving Sharesight demos at our exhibitor booth.

Meeting investors and giving Sharesight demos at our exhibitor booth.

Key takeaways

Aside from attending the conference as an exhibitor, we also had the chance to attend some of the sessions. Here are a few takeaways:

Asset Allocation for Pre-Retirees

Tim Rocks, Chief Investment Officer at E&P Financial Group:

-

Investors in the pre-retirement phase shouldn’t be concerned about the one-year performance of their portfolio. It’s important to have a timeframe for your investments that reflects the time in which you’ll need the money.

-

If you’re 40 or 50 you should be thinking about a 30-year timeframe. If you’re thinking about giving money to children or grandchildren, it’s even longer.

-

In times of volatility, it’s okay to do nothing. If your core portfolio settings are right you can just watch from the sidelines and know your portfolio is going to be okay. If you do something, make sure you are disciplined about it.

-

The worst strategy is to sell when things look bad because you’re locking in a loss. The second-worst strategy is waiting for the situation to become clearer before buying, because by that time, markets could be up 20%. You need to be disciplined when markets are strong and when they are weak.

Asset Allocation for Retirees

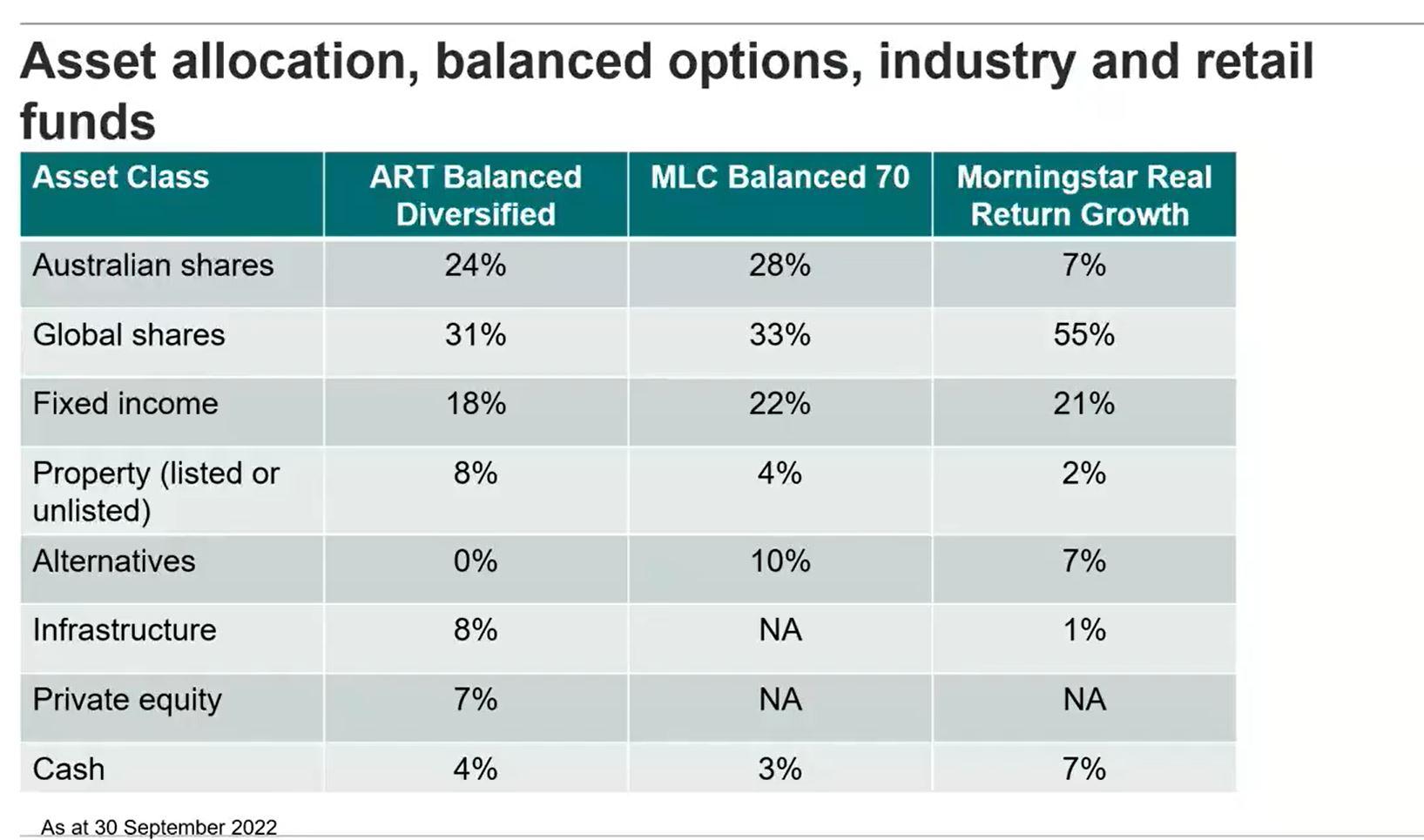

Suggested asset allocation for retirees, as proposed by the Australian Retirement Trust, MLC Asset Management and Morningstar Investment Management.

Jody Fitzgerald, Head of Institutional Portfolio Management at Morningstar Investment Solutions:

-

As a retiree, losses are more impactful because you’re drawing down on your capital and you’re not replenishing your losses.

-

Many people fear drawing down on their capital and only want to spend the money that their money makes, but this doesn’t make any sense. Think of it as cash flow management: "How do I take the assets that I have to meet my cash flow requirements?"

-

Stop thinking of your assets as income. Thinking of them this way makes people only want to invest in shares with good dividends or yielding assets, and it prevents them from considering whether or not they have overpaid for the asset.

-

For example, we’ve seen this problem with bank stocks, where a regulator could step in and stop the payment of dividends, meaning you’ve overpaid for the asset.

How Interest Rates and Inflation Impacts Portfolios

Peter Warnes, Head of Equity Research, Morningstar

-

This is the first real dose of inflation we’ve had for 20 years and markets aren’t comfortable with that because they haven’t seen that before.

-

It’s likely the RBA will stop putting rates up around the March quarter next year, but they won’t start cutting rates until the first quarter of 2024.

-

The last part of the economic cycle was in 2002, when there were low interest rates and GDP was going up. By 2003/4 the RBA started to raise rates, which they did over a 3-year period, pushing them up by 400 basis points.

-

In 2007/8 they put rates up by 225 basis points over a 2-year period. We are now seeing the move of 400 basis points in 9 months, which is the quickest it’s been since the late 1970s and early 1980s.

-

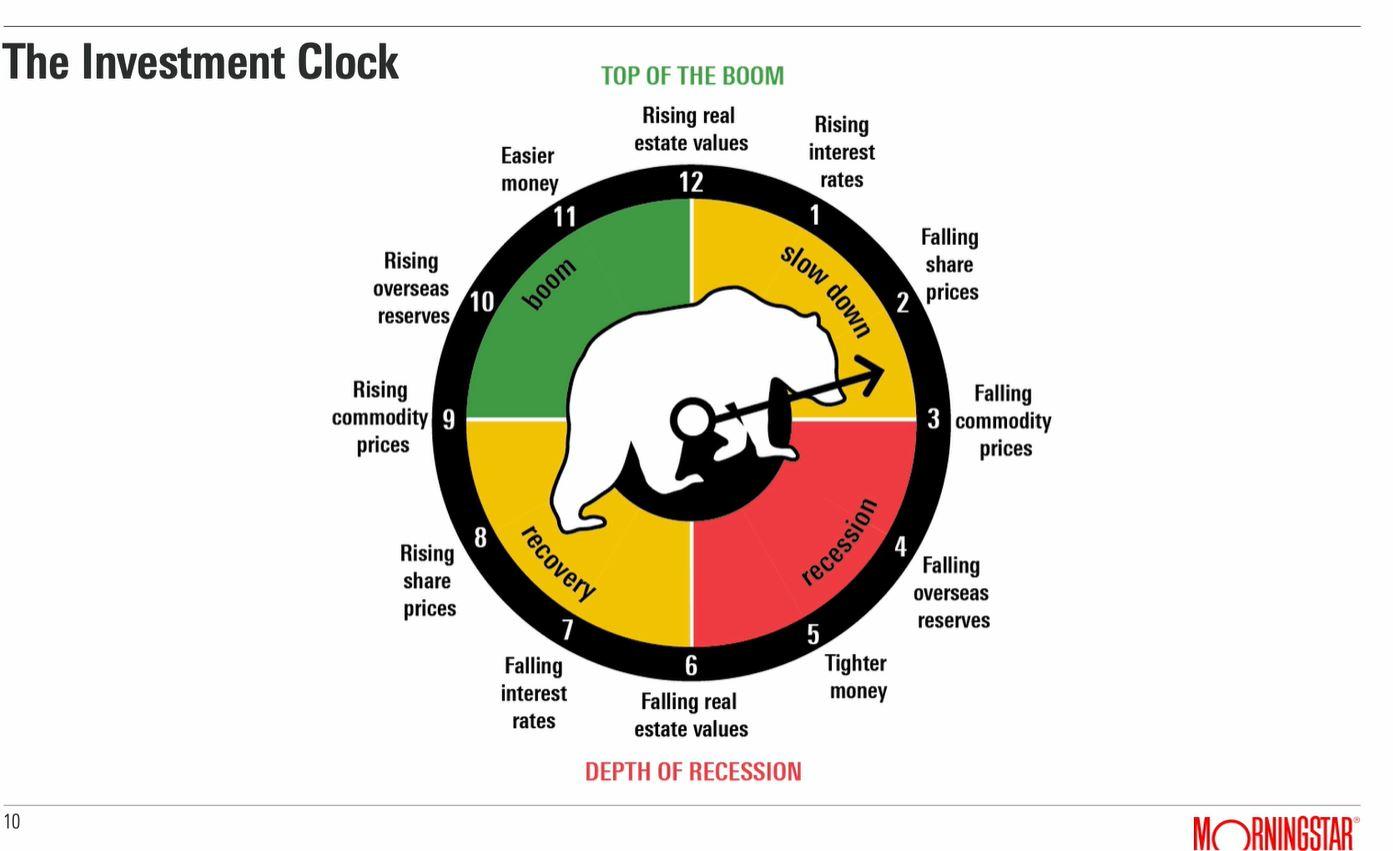

We are currently at about 2:30 on the clock. We can expect to see some extreme volatility.

-

Cash is not a balancing item in your portfolio – it’s an asset class and it gives you optionality. Cash preservation is important going into this red zone.

-

Companies that benefit from high interest rates: most insurance companies, Computershare and stocks with inflation protection like TransUrban, Aurizon, Qube, Ampol and Challenger.

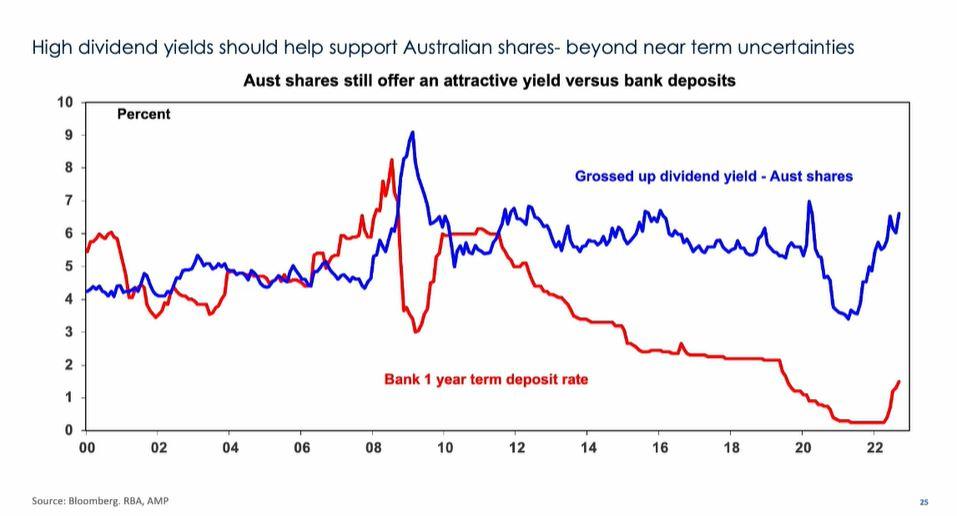

An Economist’s View of the Current Situation and How it Impacts Investors

Shane Oliver, Chief Economist at AMP Capital

-

We can expect global and Australian growth to slow to around 2% in 2023.

-

Thanks to the energy shock in Europe and aggressive central bank rate hikes, recession is now a high risk (ranging from 80% probability in Europe to 50% in the US and 40% in Australia).

-

Shares are at high risk of more weakness in the short term, but should provide reasonable returns on a 12-month view, helped by some cooling in inflation, interest rate pressures and lower price-to-earnings multiples.

-

What to watch: Supply constraints and inflation; wage growth; energy prices; the war in Ukraine; China issues; US mid-terms.

-

The tailwind to medium-term investment returns that’s been in place for the past 30-40 years (from the downtrend in inflation and interest rates) is likely now over.

-

High household debt levels will likely limit RBA rate hikes.

-

We expect the RBA to raise the cash rate to a peak of 2.85% (with an upside risk to 3.1%), ahead of rate cuts later next year.

-

Global inflation pressures may be at or close to peaking, except for Europe with its specific energy issues. This should allow central banks to ease rates later next year.

View on major asset classes over the next 12 months:

-

Cash – offers poor returns, but they are improving with rate hikes.

-

Bonds – should see some return improvement as the rise in bond yields pauses as growth and then inflation slows.

-

Shares – expect more near-term downside, but okay returns on a 12-month horizon.

-

Residential property – home prices are likely to fall 15 to 20% top to bottom into 2023 as poor affordability and rising rates have an impact, but with wide variation between regions.

-

Unlisted commercial property and infrastructure – hit by the work from home trend, online retail and rising bond yields.

-

Australian dollar – likely to remain weak with shares in the near-term, but should see a rising trend on a 12-month view as commodity prices remain strong.

Track all of your investments in one place with Sharesight

Thousands of investors like you are already using Sharesight to track the performance of their investments. If you’re not already using Sharesight, what are you waiting for? Sign up and:

-

Track all of your investments in one place, including Australian and global stocks, ETFs, mutual/managed funds, property and even cryptocurrency

-

Automatically track your dividend and distribution income from stocks, ETFs and mutual/managed funds

-

Run powerful reports built for investors, including Performance, Portfolio Diversity, Contribution Analysis, Future Income, Multi-Period and Multi-Currency Valuation

-

See the true picture of your investment performance, including the impact of brokerage fees, dividends, and capital gains with Sharesight’s annualised performance calculation methodology

Sign up for a FREE Sharesight account and get started tracking your investment performance (and tax) today.

FURTHER READING

Active vs. passive investing

What are the differences between active and passive investing, and does one offer a higher guarantee of success than the other? Keep reading to learn more.

Why Sharesight is the best multi-asset portfolio tracker

We explore how Sharesight helps you stay on top of your portfolio, optimise your performance and set yourself up for a successful year of investing.

Why tax time is so painful for family offices — and what to do about it

We discuss five reasons tax time hits family offices harder than it should, and what better infrastructure looks like in each case.