5 ways to maximise returns in a low-return world

Today, equities markets are in the very last stages of a prolonged bull cycle — the phase that saw great optimism and investor confidence is now predicted to come to a close, thanks to both the trade war tensions between the United States and China, and the impact of central banks (particularly US fed) tightening monetary policy. Both factors combined, these market conditions create an environment where lower returns are likely for investors in the short-medium term.

While lower returns are never great news, the changing market does present an opportune time to review your portfolio and your approach to look at strategies to minimise costs and maximise returns. In peak periods it is easy to ride the wave and put off assessing how we can reduce costs.

In order to maximise returns going forward, investors need to be smart about minimising investment costs. Let's explore how you can reduce costs, and maximise returns in 2019:

Take ownership of your investment decisions

The less engaged you are with your investments, the more you will need to rely on others to manage them. The costs involved in having someone else manage your investments can eat into any returns, and in a low return world, that can be significant.

Take some time to review your providers and make sure that you don't pay ongoing fees for advice that was really a one-off. Look for arrangements where you pay for the time incurred (when suppliers are doing real work for your portfolio) rather than a percentage of the portfolio for evermore.

Control your portfolio admin

Being organised with your data is another way to minimise fees; creating less work for your accountant and keeping extra cash in your pocket. Investment platforms or wraps will typically bundle in some sort of portfolio admin tools with their service, but you are paying for them in their high fees. To move away from these, you’ll want to take matters into your own hands.

Relying on your brokers’ performance figures is not ideal as they typically only report on the difference between what you paid for it and what it’s worth today. They do not take the time frame into account. A 20% return over 5 years is really only a 4% annual return. They also do not factor brokerage fees, dividends, or currency fluctuations into your return figures.

While you could create a complicated spreadsheet that handles all this, a better solution is to use a dedicated portfolio tracker such as Sharesight. It makes it easy to manage all your investments in one place, automatically calculates your total annualised return and gives you a running report of your dividend income; so you’re always aware of how you’re going.

Watch management fees

Exchange Traded Funds (ETFs) seek to emulate the returns of an index rather than trying to beat it, whereas as actively managed funds seek to do the latter, but don’t always succeed. The fees for actively managed funds are higher than passive funds, in the region of 2%+ vs 0.07-1% typically with ETFs. When equities are only returning low single digits this management cost is a significant part of your return lost.

Choosing a passive ETF can help you to bring your management fee down without making your returns suffer. In fact, most active managers fail to beat the index over longer time frames.

You can test the theory in your own portfolio within Sharesight. You can compare any holding against a common benchmark. Additionally, you can group your actively managed funds separately from your ETFs and share picks to compare and contrast which are performing better after management fees and other expenses.

Don’t pay more tax than you need to

You should be proactive and leverage tax loss selling where appropriate (and within ATO rules). Sharesight can help by calculating any unrealised capital gains in your portfolio to help you model how the resulting taxable income would impact your capital gains if particular shares were sold on the reporting date. This can help offset any capital gains you have incurred during the financial year. While many investors explore and leverage tax loss selling toward the end of the year, it is possible to harvest tax losses at any time.

The timing of your capital gains and losses is important for tax reasons. To avoid paying more tax than you need to, you should explore the impact of different allocation methods. Sharesight's Capital Gains Tax report lets investors model the impact of first-in first-out (FIFO), last-in first-out (LIFO) and other sale allocation methods on your capital gains; taking care of the math and allowing you to optimise your tax position by choosing different sale allocation methods.

Save on accounting

Managing your portfolio tax admin doesn't have to be as hard as it once was. Sharesight was built according to ATO rules and includes capital gains tax and taxable income reports that make it easy to sort out your tax obligations.

Today, you can easily prepare your own tax reports and self-file your tax return to the ATO without an accountant. Even if you choose to file the return with an accountant, having everything in order and up to date in Sharesight allows you to minimise the time and cost that would have otherwise been taken by your accountant when preparing your tax returns. And portfolio sharing capabilities let you securely share portfolio access directly with your accountant and/or financial advisor, so they have everything they need — not just at tax time, but throughout the year (so you can minimise surprises next tax season).

Taking ownership of your investment decisions, watching out for unnecessary management fees, managing your own portfolio admin and implementing strategies to ensure you aren't paying more tax than necessary, are relatively simple ways to gain back significant revenues that you may not have realised you were losing throughout this bull cycle.

Platforms like Sharesight help you to take stock of your portfolio, manage more yourself and gain a better view of which providers you need and which you can live without. Don't wait until the lower returns really kick in to assess your investment portfolio and how you can reduce your costs and maximise your returns for 2019.

Sign up for a free Sharesight account today and start maximising your investment returns.

Sharesight does not provide tax or investment advice. The buying of shares can be complex and varies by individual. Seek tax and investment advice specific to your situation before acting on any information in this article.

FURTHER READING

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

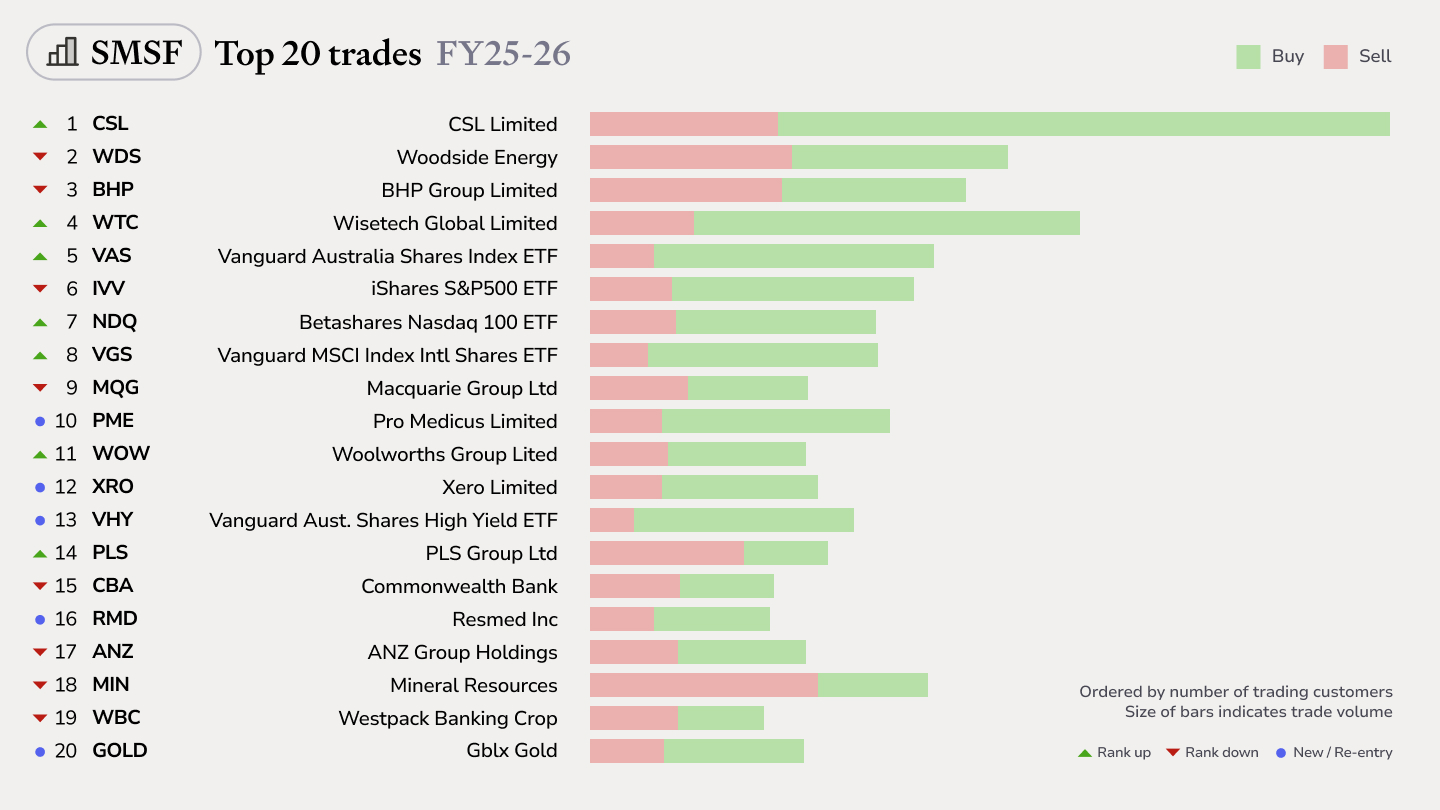

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.

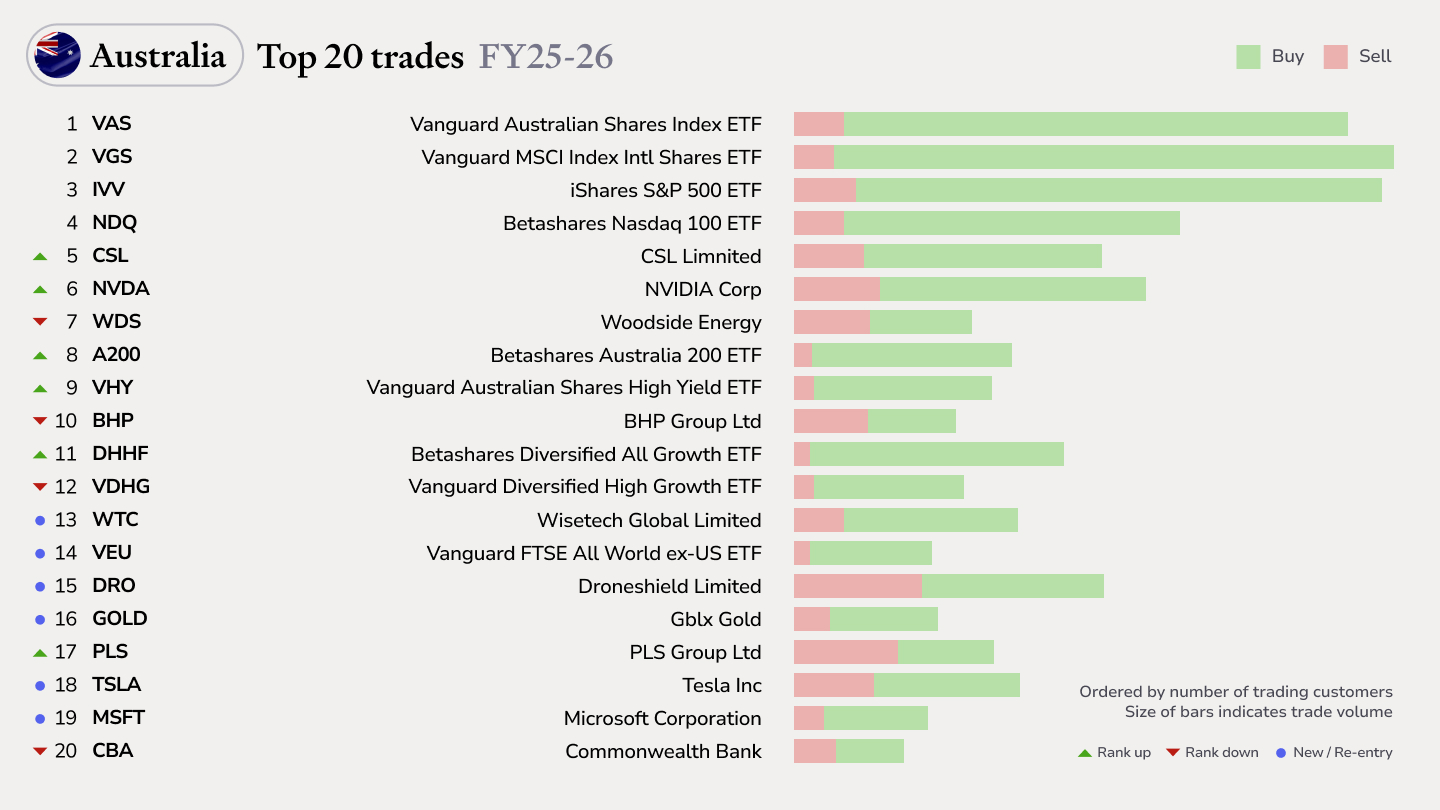

Top trades by Australian Sharesight users in FY25/26

Welcome to the FY25/26 edition of our Australian trading snapshot, where we dive into this financial year’s top trades by Sharesight users.