Tax loss selling for Australian investors

Disclaimer: The below article is for informational purposes only and does not constitute a specific product recommendation, or taxation or financial advice and should not be relied upon as such. While we use reasonable endeavours to keep the information up-to-date, we make no representation that any information is accurate or up-to-date. If you choose to make use of the content in this article, you do so at your own risk. To the extent permitted by law, we do not assume any responsibility or liability arising from or connected with your use or reliance on the content on our site. Please check with your adviser or accountant to obtain the correct advice for your situation.

Tax loss selling is a strategy that you can leverage to minimise your net capital gains earned over the financial year and reduce your income tax. While tax loss selling can be used at any time, it is most useful in the lead-up to the end of the financial year, when you have a clearer picture of your overall capital gains or losses. This makes the final months of the financial year an ideal time to review your investment portfolio and decide whether you could benefit from using this strategy to help offset your capital gains.

This article will cover:

- What is tax loss selling?

- How does tax loss selling work?

- How to model tax loss selling opportunities with Sharesight

- Avoiding wash sales

A note on the 2026-27 Federal Budget changes Under changes proposed in the 2026-27 Federal Budget, the 50% CGT discount will be replaced by cost base indexation and a 30% minimum tax rate from 1 July 2027 for individuals, trusts and partnerships. Tax loss selling itself isn't affected — you'll still be able to offset capital losses against capital gains. But the way your gain is calculated will be different from FY 2027-28 onwards. The rules covered in this article continue to apply until then.

What is tax loss selling?

Tax loss selling (or tax loss harvesting) involves selling investments that have incurred capital losses in order to “net out” or offset capital gains realised during the year. Essentially, if you wish to sell out of certain unprofitable investments in your portfolio, you may choose to use tax loss selling as a way to alleviate some of that loss and re-align your portfolio with your investing strategy, even if the net effect is still negative.

While many investors choose to leverage tax loss selling towards the end of the financial year, you can harvest losses at any time. The amount of money you save in taxes will differ depending on your tax rate (individual/trust, SMSF, company), but it should be noted that higher tax rates will apply for investments you’ve held for less than a year (short-term capital gains) than investments you’ve sold after holding them for more than a year.

How does tax loss selling work?

To help explain how tax loss selling works, let’s look at an example calculation:

Let’s say you bought 500 shares of Stock A a few years ago, when the price was $30. Today, it’s trading at $300, meaning its value has increased by $135,000. At some point, you also bought 500 shares of Stock B when the price was $100. Since then, the share price has gone down to $50, decreasing its value by $25,000.

| Holding | Purchase Value | Market Value | Capital Gain |

|---|---|---|---|

| Stock A | $15,000 | $150,000 | $135,000 |

| Stock B | $50,000 | -$25,000 | -$25,000 |

While you could hold onto Stock B in the hope that its share price will recover, you could also sell both Stock A and Stock B before the end of the financial year to offset some of the gains from your sale of Stock A with your sale of Stock B. Doing so may not only soften the impact of the loss, but it could also be a good opportunity to shed an unprofitable stock and rebalance your investment portfolio.

How to model tax loss selling opportunities with Sharesight

If you hold investments that have suffered losses this year, Sharesight’s unrealised CGT report can help you calculate how to offset your capital gains by:

- Displaying the CGT position for all your current holdings, if you were to sell them on the date of the report. These are broken down into:

- Short term capital gains (unrealised)

- Long term capital gains (unrealised)

- Capital losses (unrealised)

- Modelling the CGT that would occur across your portfolio if the shares identified were sold on the report date.

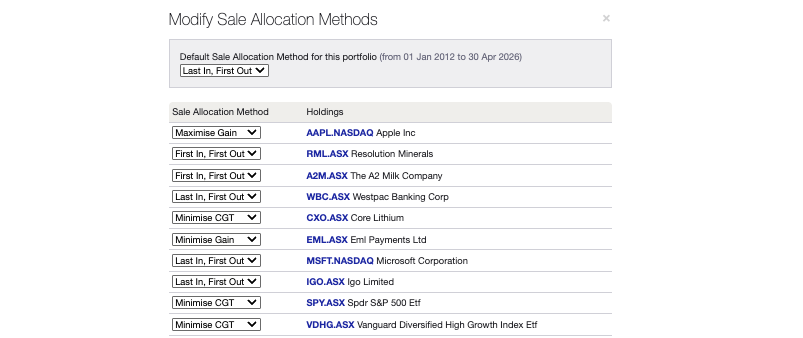

- Allowing you to modify the CGT sale allocation method at the overall portfolio or individual holding level to determine your optimal position.

Sharesight’s unrealised CGT report makes it easy to model different tax loss selling scenarios.

Sharesight’s unrealised CGT report makes it easy to model different tax loss selling scenarios.

The report uses the ‘discount method’ for shares that have been held for more than one year and the ‘other method’ for shares held for less than one year. The discount rate is based on the tax settings of an Australian portfolio:

- Individuals / Trust – CGT discount of 50 %

- Self Managed Super Fund – CGT discount of 33⅓ %

- Company – CGT discount of nil.

The report also allows you to specify the sale allocation method at the overall portfolio and individual holding level to determine your optimum position, including:

- First In, First Out (FIFO) – Sharesight assumes that you sell your longest held shares first

- Last In, First Out (LIFO) – Sharesight assumes that you sell your most recently purchased shares first

- Maximise Gain – Sharesight assumes that you sell shares with the lowest purchase price first

- Minimise Gain – Sharesight assumes that you sell shares with the highest purchase price first

- Minimise CGT – Sharesight assumes that you sell shares that will result in the lowest capital gains tax first. This method is more sophisticated than the ‘Minimise capital gain’ method because it takes into account the Australian CGT discounting rules.

Note: From 1 July 2027, the 50% CGT discount will be replaced by cost base indexation and a 30% minimum tax rate for individuals, trusts and partnerships. SMSFs (33⅓%) and companies (no discount) are unaffected. Until then, the report and the rules above continue to apply as described.

Notes on the unrealised CGT report

- The unrealised CGT report is designed for forecasting purposes only. Refer to the capital gains tax report to calculate your actual (realised) taxable capital gain income for a specific period

- You can carry forward losses from the previous reporting period by clicking on the ‘Advanced options’ link

- It’s a good idea to run the report throughout the year, not just at the end, in order to stay on top of opportunities to offset gains and losses throughout the year. You may want to share secure portfolio access with your accountant and/or adviser, so they can keep this in mind as well

- The unrealised CGT report is available on Australian standard and premium plans

- The report currently models forecasts using the existing CGT discount rules. Forecasts for sales occurring after 1 July 2027 will need to account for the new indexation method. We'll update the report as the ATO publishes guidance.

- For more information, see our instructional video below:

Avoiding wash sales

In 2008, the Australian Tax Office (ATO) issued issued tax ruling TR 2008/1, which specifically outlaws arrangements where “...in substance there is no significant change in the taxpayer’s economic exposure to, or interest in, the asset, or where that exposure or interest may be reinstated by the taxpayer”.

In other words, the ATO prevents investors from selling a stock in one financial year to take advantage of a capital loss event, only to buy that stock again in the new financial year. This is known as a “wash sale” and the ATO will disallow the loss if the sole intention of the sale was to minimise tax. As Sharesight Executive Director Andrew Bird says, “if you are going to sell, make sure you really mean it. If you still believe in that stock then choose a different ‘loser’ to sell to offset your gain”.

Calculate tax loss selling opportunities with Sharesight

Join thousands of Australian investors already using Sharesight to track their investment portfolios and optimise their CGT position. Sign up for Sharesight you can:

-

Automatically track your dividend and distribution income from stocks, ETFs, LICs and mutual/managed funds from over 60 global exchanges – including the value of franking credits

-

Use the dividend reinvestment plan (DRPs/DRIPs) feature to track the impact of DRP transactions on your performance (and tax)

-

See the true picture of your investment performance, including the impact of brokerage fees, dividends, and capital gains with Sharesight’s annualised performance calculation methodology

-

Run powerful tax reports to calculate your dividend income with the taxable income report

-

Plus calculate your CGT obligations with Sharesight’s Australian capital gains tax report and unrealised capital gains tax report

Sign up for a FREE Sharesight account and get started tracking your investment performance (and tax) today.

FURTHER READING

5 ways Sharesight helps Australian investors at tax time

Learn how Sharesight’s Australian tax features can not only help you complete your tax return, but also save you time and money at tax time.

How to present portfolio tax reports clients actually understand

Portfolio tax reports don't have to generate endless client questions. Here's how to structure them so clients can review, confirm and sign off.

Record-keeping requirements for Australian investors

Find out which records the ATO requires Australian investors to keep, and how to stay on top of your investment portfolio record-keeping with Sharesight.