Mutual funds vs. ETFs in the US

Investors often turn to mutual funds or exchange-traded funds (ETFs) when looking for broad, diversified exposure to an asset class, region or market niche, without having to buy scores of individual securities. While the concept of pooling assets for investment purposes has been around for a long time, mutual funds really captured the US public's attention in the 1980s and 1990s as stock markets boomed and investors saw record returns.

But while mutual funds have a long track record in the North American market, the ETF sector globally passed the US$10n-in-assets mark in 2021, up more than sevenfold since 2007. The growth in the US has been staggering; in 2003, there were only 123 ETFs to invest in while today there are more than 2,600 to choose from.

Mutual funds

Mutual funds are pooled investment products managed by professional fund managers. They offer investors a diversified collection of stocks and / or bonds across a range of sectors and markets in a single fund. Because the fund size is far greater than the contribution of any one investor, mutual funds offer scale, diversity, reduced risk and less exposure to market volatility than investing in a single company or industry would. Mutual funds are usually actively managed, meaning a fund manager makes decisions about how to allocate assets in the fund.

Mutual funds have traditionally appealed to "mum and dad" investors who want a simpler product and are happy to pay a premium to see their portfolio professionally managed. These investors may also be after some of the more complex features of mutual funds that aren’t available in ETFs, such as a regular cashflow or more tax efficient outcomes. The appeal of mutual funds to investors over direct investment in share markets can be summed up in three points:

-

Diversification – a range of shares, sectors and securities in one fund

-

Affordability – cheaper than directly acquiring many individual securities

-

Professional management – funds run by managers with experience and expertise.

ETFs

Like mutual funds, ETFs are a pooled investment product offering investors access to a diversified collection of stocks and other securities like bonds. Traditionally, ETFs were designed to track an index, commodity or currency, allowing investors the diversification of a mutual fund with the trading characteristics of a security that can be bought or sold on a stock exchange. Unlike mutual funds, ETFs trade like stocks and are primarily passive investments, although actively managed ETFs are also available.

ETFs tend to charge lower fees and have lower total expense ratios, or costs, than actively managed mutual funds. Passive ETFs also tend to be tax efficient, in part because tracking an index usually doesn’t require frequent trading. These products also have a structural ability to minimize the capital gains they have to distribute. While an investor who chooses a mutual fund may make a lot of money, long-term data suggest most of those who trust their money to active managers will end up worse off than if they had invested in passive vehicles such as ETFs.

ETFs, mutual funds … or something in between?

Mutual funds and ETFs have a lot in common as both consist of a mix of many different assets and represent a common way for investors to diversify. The challenge for investors is to narrow down their options. Are they best served by an ETF that tracks an index, such as the Dow Jones Industrial Average or the S&P 500, or a low-cost index mutual fund that does the same? And how to weigh the recent trend towards passive management with an actively managed mutual fund boasting stellar management and an impressive track record?

Investors should carefully consider these sorts of questions while also noting that many traditional mutual fund managers are attempting to claw back market share from ETF providers by launching actively managed ETFs. According to data providers FactSet and Ultumus, there have been 42 active ETFs listed in the US in 2020 as of June 4. This compares with just 35 index funds over the same period.

This spike in active ETFs may seem like a contradiction given the role that the ETF industry has played in undermining active management. But there are commercial reasons for the shift as the "fee war" in US index investing is having an impact on both active and passive managers.

Active vs. passive fund management

The purpose of actively managed funds is to outperform a benchmark index by selecting when to buy and sell stocks based on the fund manager's research and expertise. Actively managed mutual funds are much more common than actively managed ETFs. In both cases a fund manager is engaged to make the investment decisions although the active ETF aims to outperform a benchmark index while a mutual fund manager usually has a far broader remit to spot market irregularities to the benefit of investors. This line may become increasingly blurred in the future as the ETF industry continues to grow in complexity and seeks greater diversity in both products and investment strategies.

Mutual fund vs. ETF costs

Mutual funds are more complex products than ETFs and this translates into higher management fees. Generally, the annual cost breakdown will include an overhead or admin fee and fund manager charges. One of the advantages of an ETF is that investors can buy a diversified portfolio with the same low commission as a stock. ETFs typically have lower expense ratios than mutual funds and are generally seen as a low-cost way to earn a return similar to the index, commodity or currency being tracked.

Management fees are lower, even for more actively managed ETFs, as competition amongst providers is fierce and servicing costs are well below those of mutual funds. There is generally no minimum investment for ETFs while this can range from a few hundred to several thousand dollars for mutual funds. However, it is not a good idea to assume ETFs are always the cheapest option and investors should compare a range of ETFs and mutual funds when considering their investment options.

Mutual fund vs. ETF tax implications

ETFs are usually more tax-efficient than mutual funds. However, investors should note that this may vary according to whether the ETF is held within a taxable account or a tax-advantaged retirement account, such as an IRA or 401(k). Broadly, the sale of an ETF in the US triggers a taxable event. Whether it is a long-term or short-term capital gain or loss depends on how long the ETF was held. The cut-off point is one year: to receive long-term capital gains treatment, an investor must hold an ETF for more than one year. If they hold the security for one year or less, then it will receive short-term capital gains treatment. More about the difference between the two can be found here.

Since most ETFs are not actively managed, but follow a specific index, the underlying securities held by each unit are not generally bought and sold to trigger capital gains tax events. This means investors have more control over when they incur taxes. This means that, in general, ETF investors only face capital gains tax measures when they sell their shares while mutual fund (and actively managed ETF) shareholders may face capital gains taxes regardless of whether they sell shares. This is due to ETF shares being traded on an exchange, meaning there is a buyer for every seller. That might not be the case with a mutual fund which might need to sell shares of the underlying securities, triggering a CGT event.

Generally the rule is that actively managed funds - including actively managed ETFs - do more trading in individual stocks, which means an investor will pay much more in admin fees and CGT. Mutual funds are structured in a way that tends to incur higher capital gains taxes. Because they’re usually actively managed, the assets in a mutual fund are often bought and sold more frequently. When this is for a gain, the capital gains taxes are passed on to everyone with shares in the fund, even if you have not sold your shares.

Profiting from your investment

With both ETFs and mutual funds, investors can potentially profit in two ways. The first is the capital gain when selling out of a fund for more than you paid for it. The second is with distributions in the form of dividends, interest, capital gains or other income the fund earns on its investments.

A mutual fund offers investors the option of receiving distributions in cash or, more typically, having them reinvested in the fund. ETFs don’t reinvest cash distributions in more units or shares but rather hold this cash in the investor’s account until instructed on how it should be invested.

How to track US ETFs and mutual funds in Sharesight

Sharesight’s portfolio tracker makes it easy for US investors to keep track of all their investments in one place, with the ability to track over 24,000 US mutual funds plus thousands of other US and global ETFs and stocks.

It’s simple to add US mutual fund or ETF trades to your portfolio:

-

Sign up for a FREE Sharesight account.

-

Add your holdings to your portfolio(s) by searching for the ETF by its stock code in the relevant market, or the mutual fund’s name in the FundUS market. You can also use the Sharesight File Importer to bulk import trades to your portfolio.

-

Sharesight converts the prices and valuations of your holdings from their listed market to your portfolio’s base currency. It also automatically calculates any currency fluctuations on a daily basis and backfills past distributions (and continues to add new ones as they are announced).

Track all your mutual funds in one place

Join thousands of global investors using Sharesight to track the performance of all their investments in one place, including mutual funds. Sign up today so you can:

-

Track investments from over 40 leading global markets, including stocks, ETFs and mutual/managed funds, plus custom investments such as property and cash

-

Get the true picture of your investment performance, including the impact of brokerage fees, distributions, and capital gains with Sharesight’s annualised performance calculation methodology

-

Run powerful reports built for investors, including Performance, Portfolio Diversity, Contribution Analysis and Future Income (upcoming distributions)

-

Run tax reports including Taxable Income (dividends/distributions), Capital Gains Tax (Australia and Canada), Traders Tax (Capital Gains for traders in NZ) and FIF foreign investment fund income reports (NZ)

Sign up for a FREE Sharesight account and start tracking your investments (and tax) today.

![]()

Disclaimer: The above article is for informational purposes only and does not constitute a specific product recommendation, or taxation or financial advice and should not be relied upon as such. While we use reasonable endeavours to keep the information up-to-date, we make no representation that any information is accurate or up-to-date. If you choose to make use of the content in this article, you do so at your own risk. To the extent permitted by law, we do not assume any responsibility or liability arising from or connected with your use or reliance on the content on our site. Please check with your adviser or accountant to obtain the correct advice for your situation.

FURTHER READING

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

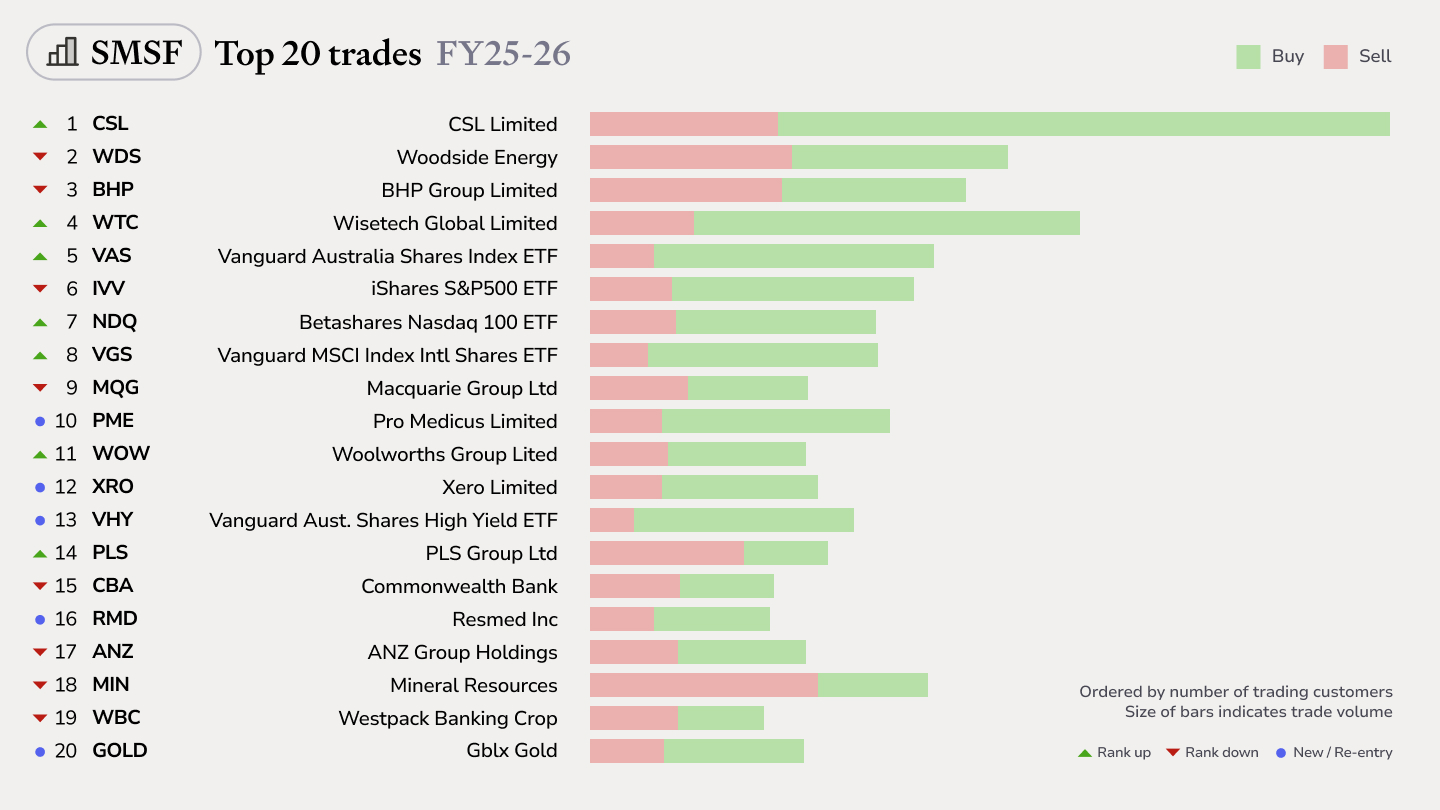

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.

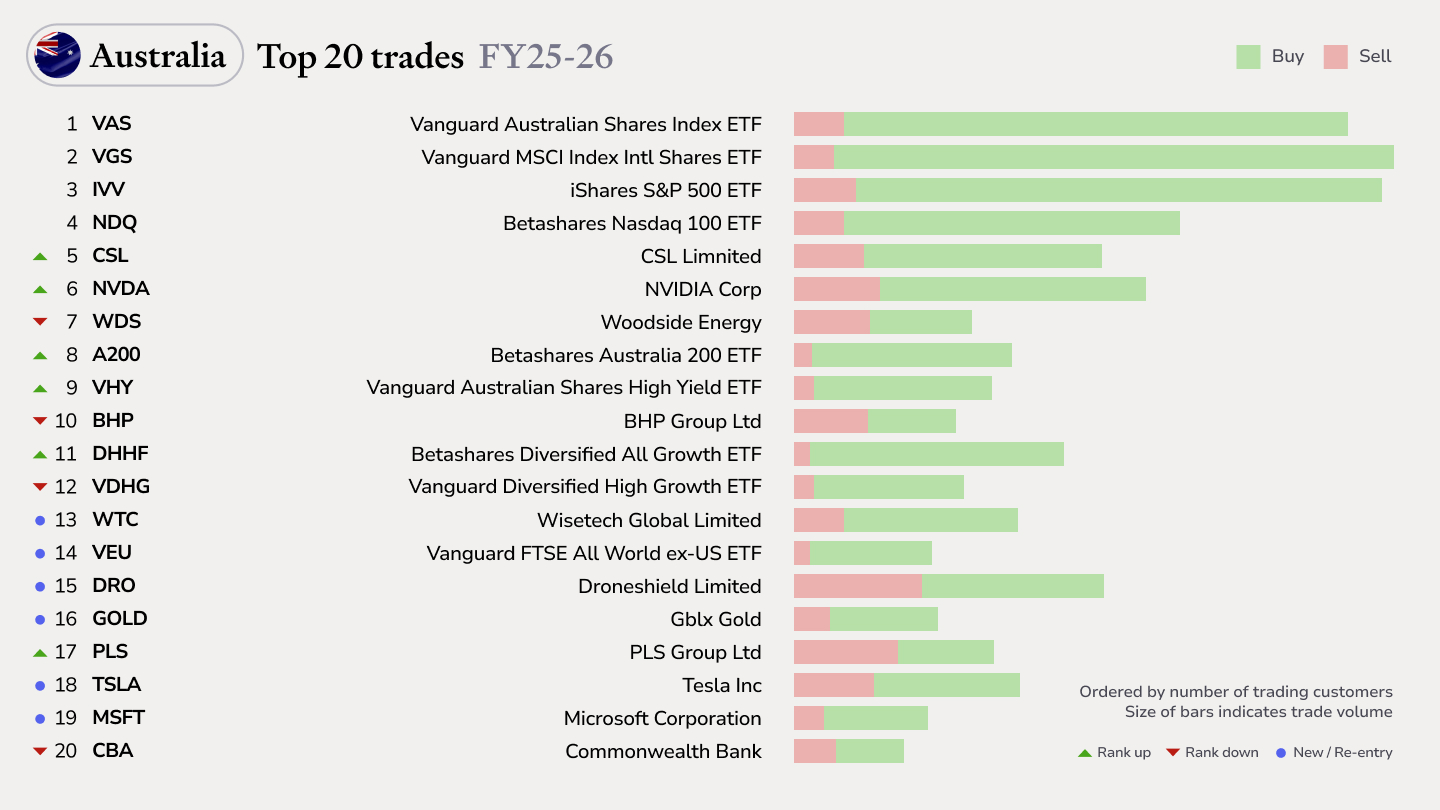

Top trades by Australian Sharesight users in FY25/26

Welcome to the FY25/26 edition of our Australian trading snapshot, where we dive into this financial year’s top trades by Sharesight users.