What is a mutual fund?

Building and managing a strong, diversified investment portfolio takes time, not to mention a good deal of investment savvy. But what if you could take a share in one that’s already been built for you? This is the opportunity given to you by a mutual fund: a portfolio shared by a pool of investors which is overseen by a professional money manager.

Mutual funds are the most popular investment vehicles for individuals who want a professionally-selected and managed portfolio, without having to pay a personal stockbroker. And while they’re generally a low-maintenance investment option with relatively few barriers to entry, they can also boast sizeable returns.

How exactly do mutual funds work?

It helps to think of a mutual fund as both an investment portfolio and a publicly owned company in its own right. Like any investment portfolio, a mutual fund is made up of stocks and bonds which fluctuate in value. However, like a publicly owned company, it’s owned by potentially thousands of investors - each of whom purchase shares in the fund itself (without voting rights, however).

Depending on the performance of the portfolio, the value of the fund goes up and down. This overall value is known as the net asset value (NAV) per share: the total value of assets in the portfolio divided by the number of outstanding shares.

Let’s consider a simplified example.

A mutual fund with $1 million worth of assets divided between 100,000 shareholders would have a NAV of $10 per share. However, if the fund performed well and its assets increased in value by 25%, the NAV would rise to $12.50 per share. Investors would therefore gain $2.50 for every unit of the fund that they own.

How do mutual fund distributions work?

While the NAV per share fluctuates up and down depending on the market, mutual funds also generate returns via dividends which are paid out on individual assets, and capital gains earned when assets are sold.

These earnings are then distributed to the mutual fund investors (after subtracting fees) on a periodic basis scheduled by the fund.

The advantages of a mutual fund

Mutual funds have grown in popularity over recent decades, laying to rest the old belief that ‘true’ investors pick their own stocks. They’re now the investment vehicle of choice for retirement plans and retail investors because of their scale and convenience.

Low barriers to entry

Mutual funds make it possible for almost anyone to invest in a secure, professionally managed portfolio. Their shares are designed to be bought easily and in small increments by retail investors, and they also open up exotic markets and instruments that are otherwise virtually impossible to negotiate unless you’re an investment professional.

Choice

Mutual funds come in all shapes and sizes, so there’s something to suit almost every investment objective. Some are targeted to different asset classes (e.g. bond funds), while others invest primarily in particular market sectors or industries. The money managers of each fund also have their own investment styles, such as growth investing, value investing, or macroeconomic investing.

Instant diversification

Building and measuring a properly diversified portfolio from scratch takes time, but mutual funds can give you instant exposure to a wide variety of uncorrelated assets – making for a favourable risk/return ratio with a minimum of fuss.

Lower transaction fees

Buying individual stocks one at a time means multiple transaction fees, which quickly add up. With a mutual fund, however, investors pay one fee for exposure to potentially hundreds of assets.

Professional management

Prior to mutual funds, only the wealthiest investors could afford to have their assets managed by a private money manager. Mutual funds, however, give everyday retail investors the opportunity to have their assets professionally managed for a relatively small fee.

The disadvantages of a mutual fund

While the easily accessible nature of mutual funds makes them well suited to anyone who favours a more passive, low maintenance investing approach, they do have their downsides. This is particularly true for investors who have a higher risk tolerance.

Over diversification

The average mutual fund invests in at least 100 different assets. While this diverse spread generally allows mutual funds to ride out even intense market volatility, it can also diminish their expected rate of return – because the losses and gains across different asset categories begin to offset one another.

Uninvested cash

A sizeable portion of the portfolio tends to be kept as cash, so the fund is never caught short when investors want to withdraw. While this guarantees liquidity, it also means that a chunk of each investment sits in the fund as cash with no chance of generating a return.

Choosing a fund

Choosing between the many mutual funds available can be difficult, especially because performance metrics such as earnings per share (EPS) aren’t available for funds as they are for equities. Moreover, the different investment styles and focuses of each fund make them difficult to compare.

Variable performance

Actively managed funds are controlled by a money manager, but there’s no guarantee that their performance will be better than market average – or better than what you’d get if you managed it yourself. Fees still apply regardless of performance however, and individual investors have no say in trading decisions.

Performance fees

While it’s cheaper than hiring a private money manager, mutual funds aren’t run for free. Investors generally pay an annual operating fee of 1-3% of the total funds under management plus costs associated with individual transactions.

Can mutual funds lose money?

Like any investment vehicle that relies on assets with fluctuating value, mutual funds can lose money. However, given their diversification and professional management, they’re generally a safer choice for novice investors than building a portfolio from scratch.

Track all your mutual funds in one place

Join thousands of global investors using Sharesight to track the performance of all their investments in one place, including mutual funds. Sign up today so you can:

-

Track investments from over 40 leading global markets, including stocks, ETFs and mutual/managed funds, plus custom investments such as property and cash

-

Get the true picture of your investment performance, including the impact of brokerage fees, distributions, and capital gains with Sharesight’s annualised performance calculation methodology

-

Run powerful reports built for investors, including Performance, Portfolio Diversity, Contribution Analysis and Future Income (upcoming distributions)

-

Run tax reports including Taxable Income (dividends/distributions), Capital Gains Tax (Australia and Canada), Traders Tax (Capital Gains for traders in NZ) and FIF foreign investment fund income reports (NZ)

Sign up for a FREE Sharesight account and start tracking your investments (and tax) today.

Disclaimer: The above article is for informational purposes only and does not constitute a specific product recommendation, or taxation or financial advice and should not be relied upon as such. While we use reasonable endeavours to keep the information up-to-date, we make no representation that any information is accurate or up-to-date. If you choose to make use of the content in this article, you do so at your own risk. To the extent permitted by law, we do not assume any responsibility or liability arising from or connected with your use or reliance on the content on our site. Please check with your adviser or accountant to obtain the correct advice for your situation.

FURTHER READING

Save time and money by sharing your portfolio with your accountant

It's easy to save time and money at tax time by sharing access to your Sharesight portfolio with your accountant. Keep reading to learn more.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

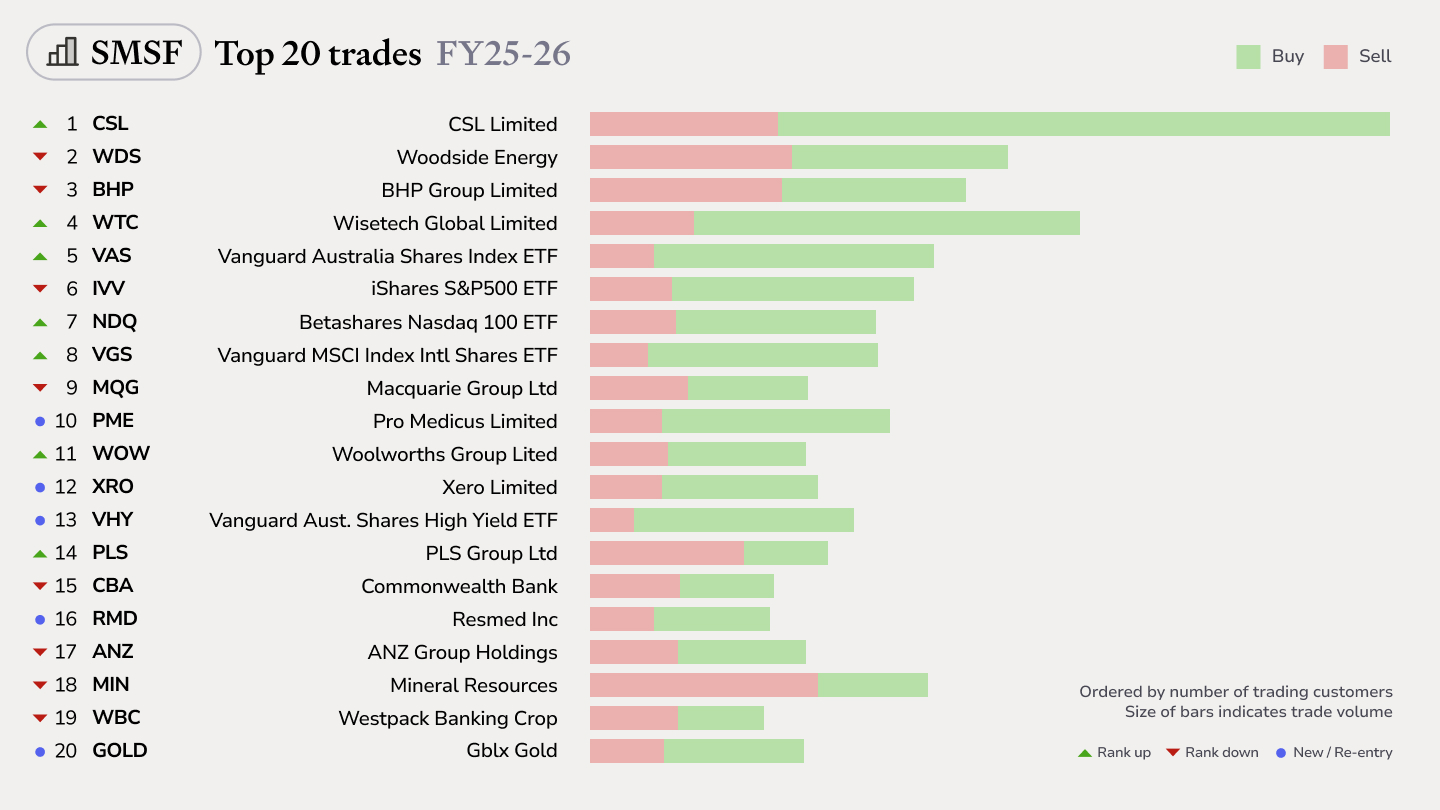

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.