What is an Australian investment bond?

Disclaimer: The below article is for informational purposes only and does not constitute a product recommendation, or taxation or financial advice and should not be relied upon as such. Please check with your adviser or accountant to obtain the correct advice for your situation.

An investment bond is similar to a managed fund -- but is typically sold through insurance and mutual companies (like AMP, Australian Unity, GenLife, etc). Investment bonds can be a tax-effective way to save for something big over the long term -- like your children’s or grandchildren's education, because earnings on the investment are tax free and do not need to be included in assessable income when held for more than 10 years.

Investment bonds are different to corporate or government bonds, which represent a loan from an investor to a borrower (such as a corporation or government entity) and will receive a regular payment at a fixed interest rate.

Investment bonds, like managed funds, offer investments in a range of underlying assets:

-

Australian shares

-

International shares

-

Property

-

Cash

-

Fixed interest

-

Infrastructure

-

Diversified funds

Investment bonds are a type of investment-savings plan, and because earnings are taxed within the bond at 30%, they’re considered ‘tax-paid’ investments at the company tax rate of 30% -- making them attractive to investors on higher marginal tax rates.

Investment bonds 10 year rule

In order to take advantage of the income tax exemption for withdrawal or sale of the units in the investment bond, you must keep the contributions invested for at least 10 years. If you decide to withdraw any amount before the 10 year period, either some or all of the income may be assessable, subject to a 30% offset for tax already paid on earnings by the company.

Investment bonds 125% rule

One of the major benefits of investment bonds is that you can ‘top up’ the money invested in the bond on a yearly basis (investing a maximum of 125% more than each previous year) and still pay no capital gains on these subsequent contributions when the capital gains tax exception applies to the initial investment.

Investors need to be mindful however, because the 10 year capital gains tax exemption period resets whenever contributions are paused for more than a year and then followed by further contributions, or where contributions exceed 125% of the previous year’s investment.

The table below illustrates a case where an investor is able to contribute up to $89,407 by year 10 by starting at $12,000/year or $1000 per month.

| Year | Contribution amount |

| 1 | $12,000 |

| 2 | $15,000 |

| 3 | $18,750 |

| 4 | $23,438 |

| 5 | $29,297 |

| 6 | $36,621 |

| 7 | $45,776 |

| 8 | $57,220 |

| 9 | $71,526 |

| 10 | $89,407 |

Investment bonds are for the long term

The main points to keep in mind when considering an investment bond are:

-

It’s for the long term

-

It can be tax effective

-

It’s most suited to people on a marginal tax rate higher than 30%

-

It’s can be used to save for your children’s or grandchildren’s education

-

It’s also a tool for estate planning

-

It has a beneficiary eg., children or grandchildren. In the unfortunate event of the investment holder passing away, the money goes to the nominee tax-free

-

It attracts management fees

How do I track investment bond performance?

Like many vehicles in the investment world and like many superannuation funds, when you login to your investment bond provider’s online portal, you can see the amounts contributed into the underlying instruments.

For example, a transaction statement from Australian Unity Lifeplan investment bond looks like this:

I can log in and see pages of these contributions into the investment bond. But I don’t get to see how the investment bonds are actually performing, despite, the underlying instruments being unitised funds.

Using Sharesight to track performance of investment bonds

It’s easy to search for the underlying unitised fund within investment bonds like this by manually searching for the fund code in Sharesight.

Personally, I then use the "Custom Group" feature to group these unitised investments into a single group to identify the investment bond instrument. Below is a screenshot from the Overview page of Sharesight where I have set it up as a Custom Group.

Alternatively, because of the preferred tax treatment of these bonds, you could set up a distinct Sharesight portfolio to hold these, to separate out the impact of capital gains in these from the rest of your investments.

Track your investment bonds today

It’s easy to track investment bonds like these with Sharesight, sign-up to Sharesight for free, built for the needs of Australian investors:

- Get the true picture of your investment performance, including the impact of brokerage fees, dividends, and capital gains with Sharesight’s annualised performance calculation methodology

- Sharesight automatically tracks your daily price & currency fluctuations, as well as handles corporate actions such as dividends, franking credits and share splits

- Run powerful tax reports built for investors, including Capital Gains Tax and Unrealised Capital Gains Tax

FURTHER READING

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

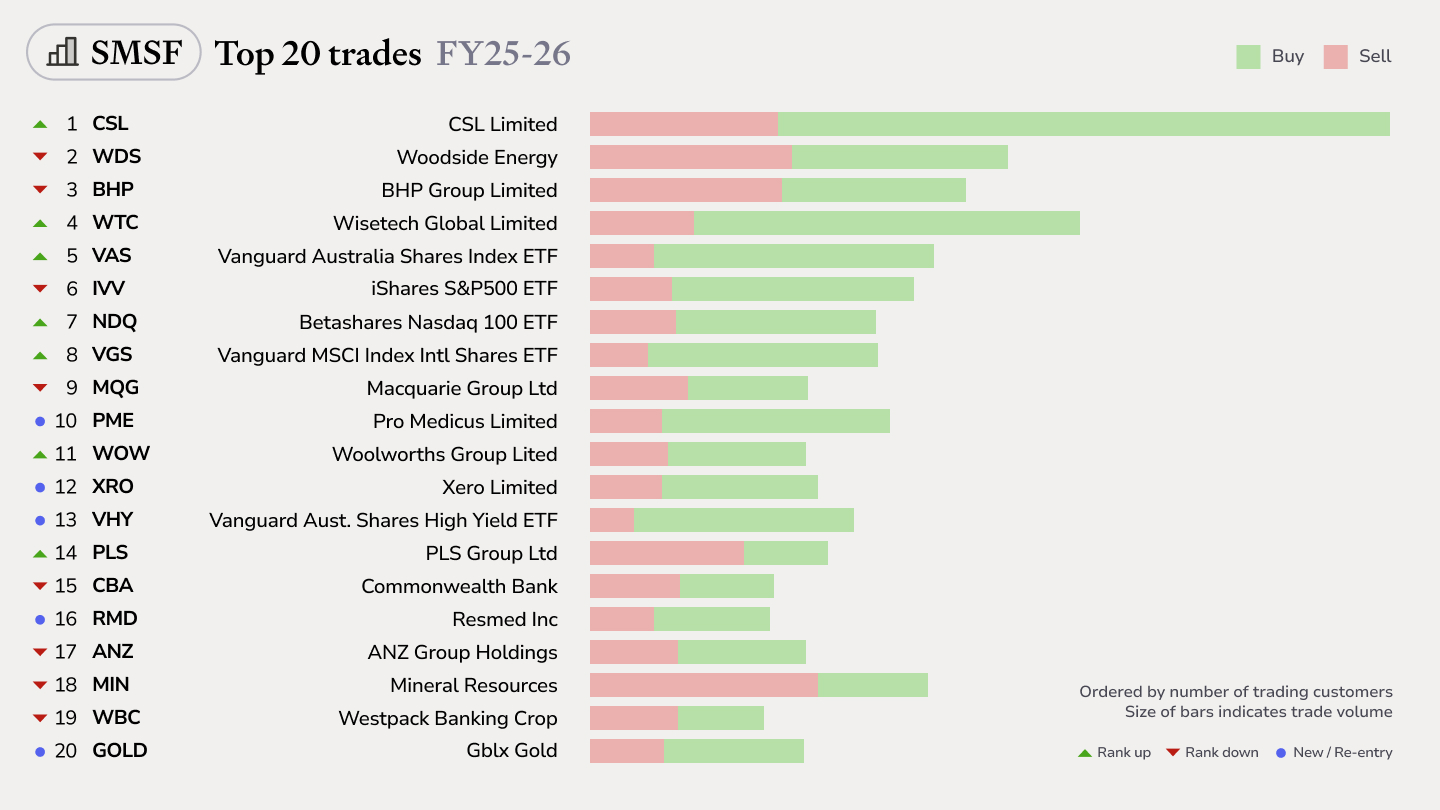

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.

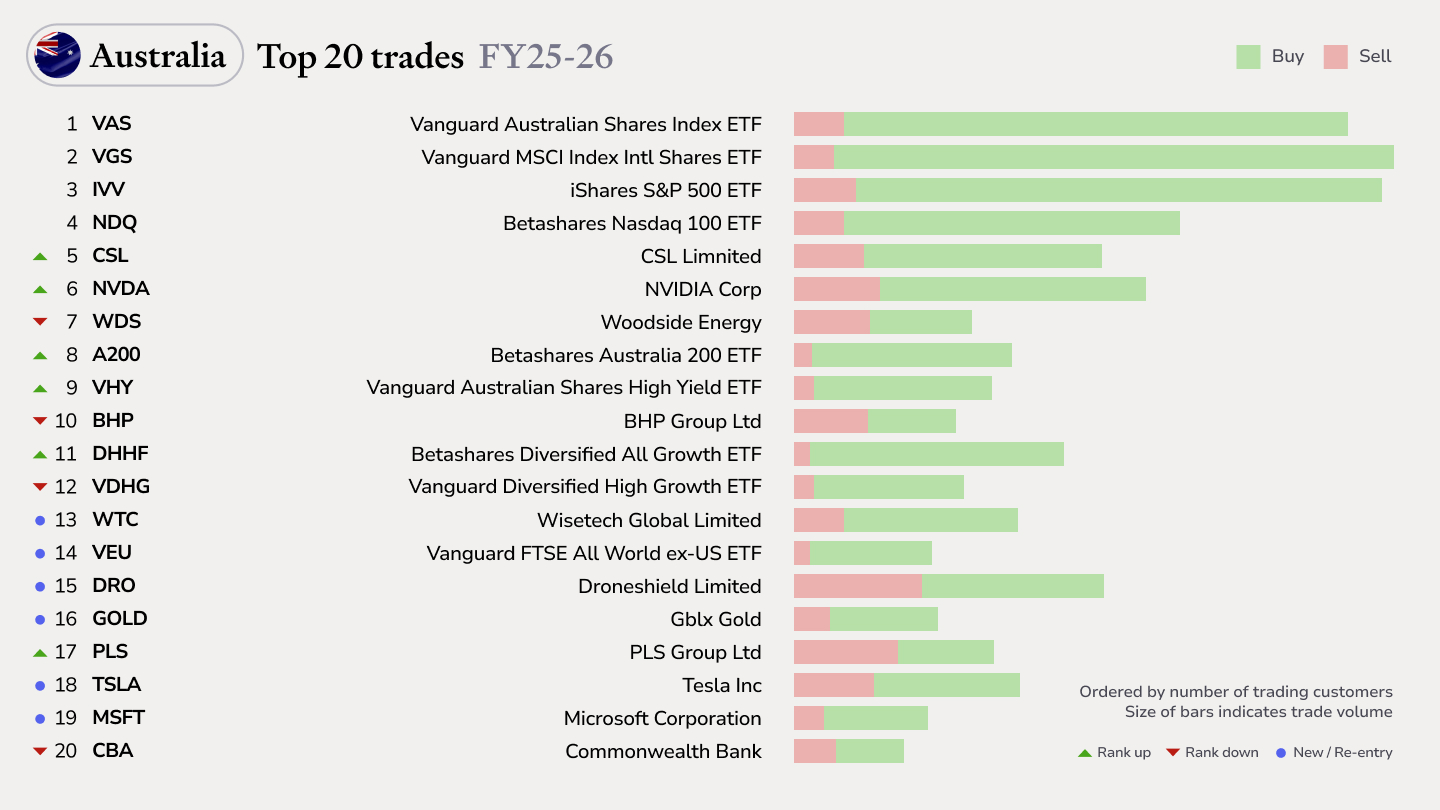

Top trades by Australian Sharesight users in FY25/26

Welcome to the FY25/26 edition of our Australian trading snapshot, where we dive into this financial year’s top trades by Sharesight users.